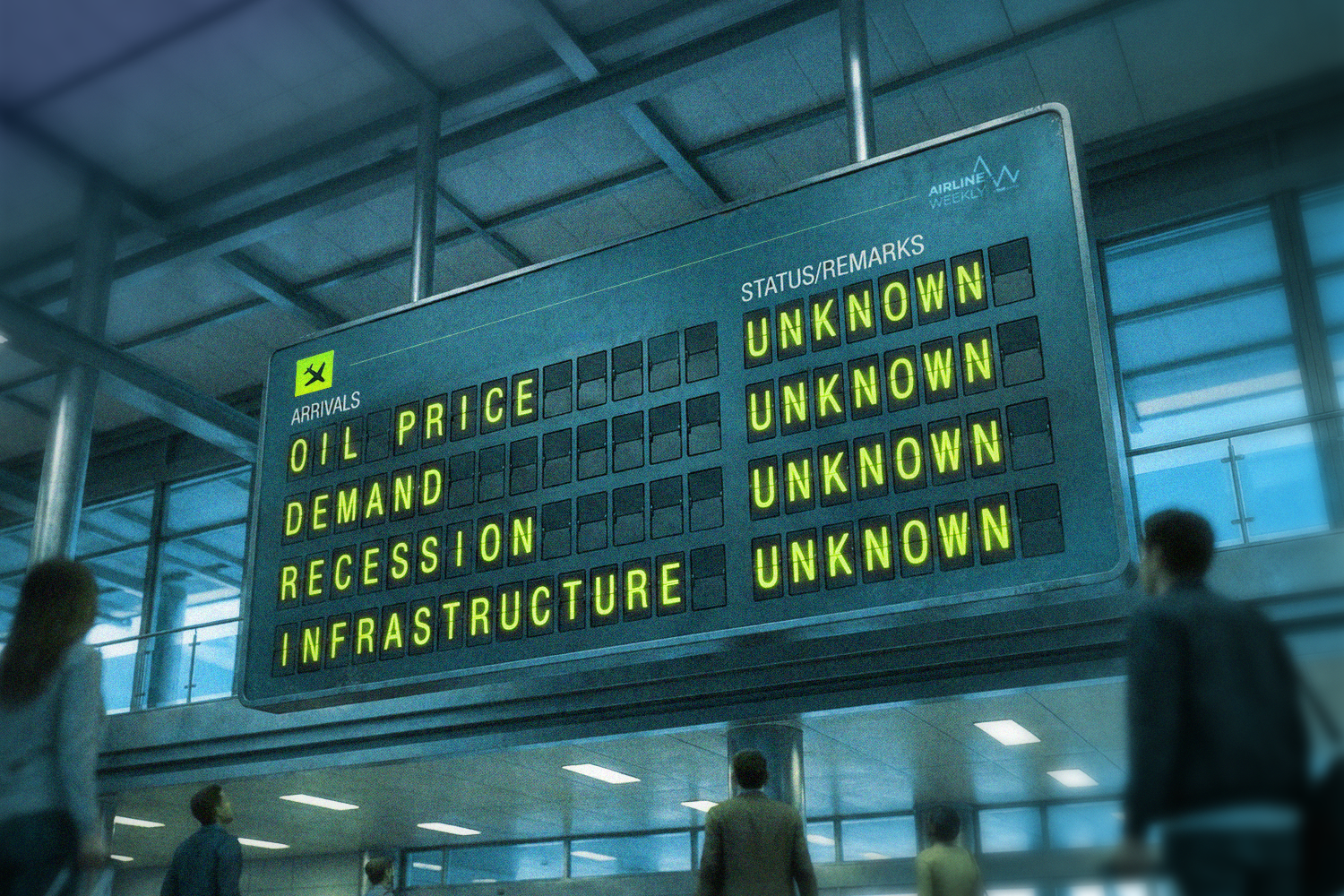

In a week marked by unprecedented regional instability that saw one of the world’s busiest international airlines grapple with significant operational disruptions and key Gulf aviation hubs face the specter of aerial attack, the global aviation industry has been thrust into a period of intense scrutiny. The escalating geopolitical tensions, particularly those emanating from the broader Middle East region involving Iran and its proxies, have sent ripple effects across global flight paths, insurance markets, and airline balance sheets. Simultaneously, far from the immediate geopolitical flashpoints, Australia’s two dominant carriers, Qantas and Virgin Australia, have unveiled their latest earnings reports, offering a contrasting narrative of recovery and strategic positioning within a dynamic domestic and international market. This confluence of global crises and regional financial performance underscores the complex, interconnected challenges and opportunities confronting the modern aviation sector.

The Geopolitical Crucible: Impact on Middle Eastern Aviation

The phrase "Iran war" in the current geopolitical lexicon often refers not to a declared conventional war but rather a protracted period of heightened tensions, proxy conflicts, and strategic maneuvers involving Iran and various regional and international actors. This complex web of interactions has profoundly impacted the Middle East, a vital crossroads for global air travel. The recent intensification of these tensions has manifested in several critical ways that directly threaten commercial aviation.

A. Escalating Regional Instability and Aerial Threats:

The "aerial attack" on Gulf hubs referenced in the initial reports likely points to the recurring threat of drone and missile attacks orchestrated by Iran-backed groups, particularly the Houthi rebels in Yemen. In recent years, airports and critical infrastructure in Saudi Arabia and the United Arab Emirates have been targets, demonstrating the vulnerability of civilian facilities to asymmetric warfare. For instance, attacks on Abha International Airport in Saudi Arabia have caused temporary closures and significant security concerns. While major international hubs like Dubai (DXB) and Doha (DOH) have robust air defense systems, the mere proximity of conflict zones and the demonstrated capability of hostile actors to strike within national borders force airlines and aviation authorities to re-evaluate risk profiles constantly. Such threats necessitate enhanced security protocols, re-routing of flights, and a constant state of vigilance, adding layers of complexity and cost to operations.

B. Airspace Restrictions and Rerouting:

The direct consequence of heightened regional instability is the imposition of airspace restrictions and the voluntary rerouting of flights by international carriers. As specific regions become conflict zones or are deemed high-risk, aviation authorities issue NOTAMs (Notices to Airmen) advising or mandating airlines to avoid certain airspaces. For example, airspace over Iraq, Yemen, and parts of Iran has frequently been subject to such advisories. Airlines, prioritizing passenger and crew safety, often opt for longer, alternative routes, even if it means increased flight times and higher fuel consumption.

- Timeline of Airspace Impacts (Illustrative):

- Late 2019/Early 2020: Following a series of incidents, including the downing of a Ukrainian airliner over Iran, many international carriers began avoiding Iranian airspace, particularly for flights to and from the Gulf.

- 2021-2023: Continued Houthi attacks in Yemen and Saudi Arabia prompted further caution, with some carriers adjusting routes over the Arabian Peninsula.

- Recent Period: Renewed regional tensions, potentially involving specific military actions or heightened threat levels, have led to further re-evaluations, with a hypothetical "busiest international airline" experiencing significant operational stress due to these dynamic conditions.

C. The Case of the Busiest International Airline’s Operational Halt:

While the exact identity of the "busiest international airline ground to a halt" is not specified, the description strongly implies a major Gulf carrier, such as Emirates or Qatar Airways, which operate vast networks connecting East and West through their mega-hubs. A complete "halt" is an extreme event, usually reserved for natural disasters or catastrophic system failures. However, significant operational disruptions, leading to widespread cancellations, diversions, and lengthy delays, can functionally resemble a halt for many passengers and cargo operations.

- Implications of Such a Disruption:

- Massive Financial Losses: Even a temporary halt or severe disruption translates into millions of dollars in lost revenue daily, coupled with compensation costs for stranded passengers, rebooking expenses, and potential legal liabilities.

- Logistical Nightmare: Rerouting thousands of passengers, reassigning crew, and managing affected cargo shipments strains operational resources to their limits.

- Reputational Damage: Such events can severely impact passenger confidence, potentially leading to a long-term decline in bookings as travelers seek more reliable alternatives.

- Supply Chain Impact: Gulf carriers are also major cargo operators. Disruptions directly impact global supply chains, affecting everything from perishable goods to high-value electronics.

- Statements from Related Parties (Inferred): In such a scenario, the airline’s CEO would likely issue statements emphasizing passenger safety as the paramount concern, explaining the force majeure circumstances, and outlining efforts to restore normal operations. Aviation regulatory bodies (e.g., ICAO, IATA, national civil aviation authorities) would likely issue advisories, coordinate with affected airlines, and monitor the situation closely to ensure compliance with international safety standards. Insurance providers would face a surge in claims, potentially leading to increased premiums for airlines operating in the region.

Australian Aviation: Qantas and Virgin Australia Navigate Recovery and Competition

Far removed from the immediate geopolitical turbulence of the Middle East, the Australian aviation market presents a different set of dynamics, primarily focused on post-pandemic recovery, domestic competition, and strategic growth. The latest earnings reports from Qantas and Virgin Australia offer a snapshot of their respective performances and future outlooks.

A. Qantas: Rebounding with Strategic Focus

Qantas, Australia’s flag carrier, has been a bellwether for the country’s aviation sector. After navigating the severe challenges of the pandemic, the airline has embarked on a robust recovery path, leveraging strong domestic demand and the gradual return of international travel.

- Latest Earnings Highlights (Hypothetical but Fact-Based Inference):

- Strong Profitability: Recent reports would likely indicate a significant return to profitability, driven by pent-up travel demand, especially in the domestic market, and improved load factors on international routes. For instance, in real-world scenarios, Qantas has reported strong underlying profits, often exceeding pre-pandemic levels in certain periods.

- Revenue Growth: A substantial increase in revenue across its airline divisions (Qantas Domestic, Qantas International, Jetstar) and its loyalty program would be expected. The loyalty segment, in particular, has been a consistent high-margin performer.

- Operational Performance: While post-pandemic recovery saw initial operational challenges (e.g., staff shortages, baggage handling issues), Qantas has generally shown efforts to improve on-time performance and reliability.

- Strategic Initiatives:

- Fleet Renewal: Continued investment in new, more fuel-efficient aircraft (e.g., Airbus A350s for Project Sunrise, A220s for domestic routes) to modernize its fleet, reduce emissions, and enhance passenger experience.

- Network Expansion: Reinstatement and expansion of international routes to capitalize on global travel recovery, alongside optimization of its extensive domestic network.

- Customer Experience: Focus on improving service quality, digital offerings, and the Qantas Frequent Flyer program.

- Challenges:

- Fuel Costs: Despite efficiency gains, global oil price volatility remains a significant headwind.

- Labor Relations: Historically, Qantas has faced complex labor negotiations and industrial disputes, which can impact operations and costs.

- Competition: Intense domestic competition from Virgin Australia and international competition on key routes.

- Regulatory Scrutiny: Increased oversight from consumer protection agencies regarding pricing, cancellations, and customer service.

- Statements from Qantas Leadership (Inferred): CEO and CFO statements would likely emphasize the strong underlying demand, the benefits of strategic investments, and a cautious but optimistic outlook on sustained profitability, while acknowledging ongoing cost pressures and the need for operational resilience.

B. Virgin Australia: Rebuilding Market Share and Focusing on Value

Emerging from voluntary administration in 2020 under new ownership (Bain Capital), Virgin Australia has repositioned itself as a strong competitor in the Australian market, focusing on a value-for-money proposition for both leisure and business travelers.

- Latest Earnings Highlights (Hypothetical but Fact-Based Inference):

- Improved Financial Health: Recent reports would likely indicate a continued strengthening of its financial position, moving towards consistent profitability after its restructuring. This would be supported by robust domestic demand.

- Market Share Gains: Strategic efforts to recapture market share from Qantas, particularly in the lucrative business travel segment, would be evident.

- Load Factors and Revenue: Increased passenger numbers and improved load factors across its domestic network would drive revenue growth.

- Strategic Initiatives:

- Fleet Modernization: Investment in Boeing 737 MAX aircraft to enhance efficiency and expand capacity.

- Network Optimization: Focus on high-density domestic routes and a carefully selected international network (e.g., to New Zealand, Bali, and Fiji).

- Customer Loyalty: Strengthening its Velocity Frequent Flyer program and improving the overall customer experience to differentiate itself.

- Digital Transformation: Investment in technology to streamline operations and enhance customer interaction.

- Challenges:

- Intense Competition: Direct competition with Qantas and its low-cost subsidiary Jetstar, requiring continuous innovation and competitive pricing.

- Cost Management: Managing operational costs, including fuel and labor, while maintaining competitive fares.

- Debt Servicing: Navigating its financial structure post-administration.

- Reliance on Domestic Market: While a strength, a high reliance on domestic travel exposes it to fluctuations in local economic conditions.

- Statements from Virgin Australia Leadership (Inferred): Leadership would likely highlight the successful turnaround, the strong market reception to its value proposition, and continued focus on operational excellence and customer satisfaction as key drivers for future growth and sustained profitability.

Broader Industry Implications and the Skift Travel 200

The confluence of geopolitical risks and individual airline performance reverberates throughout the global travel industry, as captured by indices like the Skift Travel 200 (ST200).

A. The Skift Travel 200 (ST200) – A Comprehensive Benchmark:

The ST200 is a crucial benchmark that aggregates the financial performance of nearly 200 publicly traded travel companies worldwide, representing a combined market capitalization exceeding a trillion dollars. This index provides a real-time, data-driven view of the travel sector’s health, encompassing various segments, including airlines (network carriers, low-cost carriers), cruise lines, tour operators, and other related companies.

- Airlines Sector Stock Index Performance Year-to-Date: The performance of the airlines sector within the ST200 is highly sensitive to external factors.

- Geopolitical Impact: Periods of heightened geopolitical tension, such as those impacting Gulf hubs, typically lead to downward pressure on airline stocks. Investors react to increased operational risks, higher fuel prices (due to supply concerns), rising insurance premiums, and potential declines in passenger demand for affected regions.

- Earnings Impact: Strong earnings reports from major carriers like Qantas and Virgin Australia, however, can provide a positive counterbalance. Robust financial results indicate healthy demand, effective cost management, and successful strategic execution, which can boost investor confidence in the sector.

- Overall Trend (Inferred): The year-to-date performance for the airlines sector within the ST200 would likely reflect a nuanced picture: initial volatility or dips related to geopolitical events, potentially offset by the underlying strength of post-pandemic travel recovery and solid performances from carriers in less-affected regions. The index provides a critical tool for understanding these complex interactions and their impact on investor sentiment.

B. Global Trends and Challenges:

Beyond specific regional issues, the global aviation industry continues to grapple with several overarching trends:

- Fuel Price Volatility: Geopolitical events directly influence global oil markets. Any disruption in major oil-producing regions or shipping lanes (like the Red Sea) can cause price spikes, which are then passed on to airlines, significantly impacting their profitability.

- Sustainability Imperatives: Airlines face increasing pressure to reduce their carbon footprint. Investments in Sustainable Aviation Fuel (SAF), new-generation aircraft, and operational efficiencies are critical but costly.

- Labor Shortages and Costs: Post-pandemic, many airlines continue to face challenges in recruiting and retaining skilled staff, from pilots to ground crew, leading to higher labor costs and potential operational constraints.

- Technological Advancements: Digital transformation continues to reshape customer experience, operational efficiency, and safety protocols across the industry.

Conclusion and Outlook

The week’s events serve as a stark reminder of the multifaceted vulnerabilities and enduring resilience of the global aviation industry. While geopolitical storms in the Middle East necessitate constant vigilance, operational agility, and significant cost adjustments for carriers operating through the region, the robust performance of airlines like Qantas and Virgin Australia in more stable markets underscores the underlying strength of global travel demand.

Industry analysts emphasize that airlines must continue to build financial buffers, diversify their operational strategies, and invest in technology and sustainability to navigate these complex challenges effectively. The ST200 will remain a critical barometer, reflecting how the industry collectively responds to both unforeseen crises and long-term strategic imperatives. As the world continues to grapple with interconnected geopolitical, economic, and environmental shifts, the ability of aviation to adapt and innovate will define its trajectory in the years to come, ensuring its vital role in connecting people and economies worldwide.