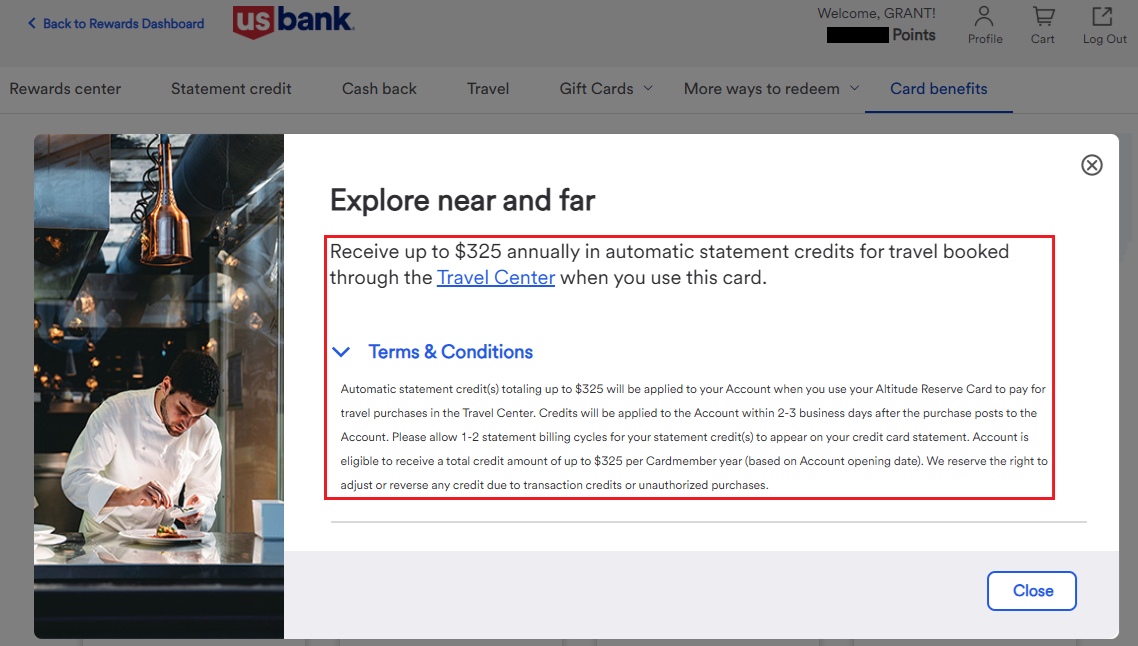

The landscape of premium travel credit cards continues to shift as major financial institutions refine their reward structures and redemption requirements, a trend exemplified by the recent adjustments to the US Bank Altitude Reserve Credit Card. Central to this evolution is the administration of the $325 annual travel credit, a cornerstone benefit that has recently undergone a significant transition in its application process. While previously accessible through direct travel purchases, the credit now necessitates utilization through the proprietary US Bank Travel Center, a move that mirrors broader industry trends toward centralized travel ecosystems. This structural change was recently highlighted through a documented redemption sequence involving a multi-night hotel reservation, providing a clear window into the efficiency and mechanics of the current system.

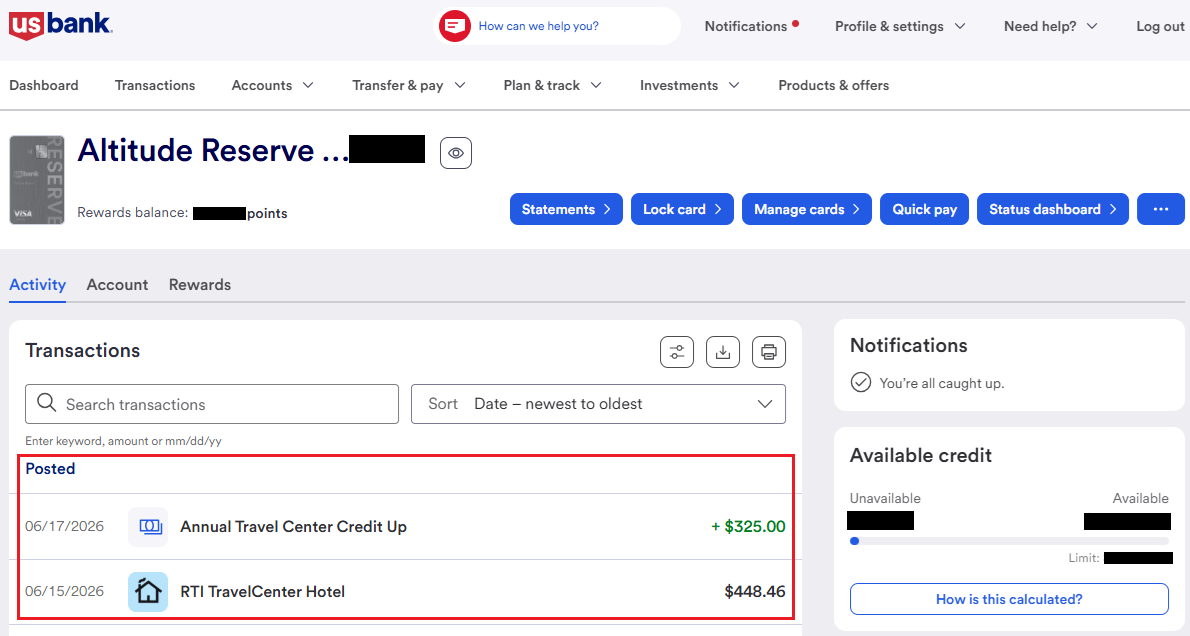

The US Bank Altitude Reserve, positioned as a high-tier competitor to the Chase Sapphire Reserve and the American Express Platinum Card, carries a $400 annual fee. To offset this cost, the card offers a $325 annual credit for eligible travel and dining purchases. In the current fiscal cycle, cardholders have observed that the seamless integration of this credit now relies on the bank’s internal booking infrastructure. A recent transaction recorded on June 14 involved a two-night hotel stay totaling $448. This booking, facilitated through the US Bank Travel Center, served as the catalyst for the $325 credit reimbursement. The timeline of this transaction underscores the automated nature of the bank’s backend systems; within four days of the initial booking, the $325 credit was officially posted to the account on June 18, significantly ahead of the standard 1-2 billing cycle window often cited in cardmember agreements.

Chronological Breakdown of the Redemption Process

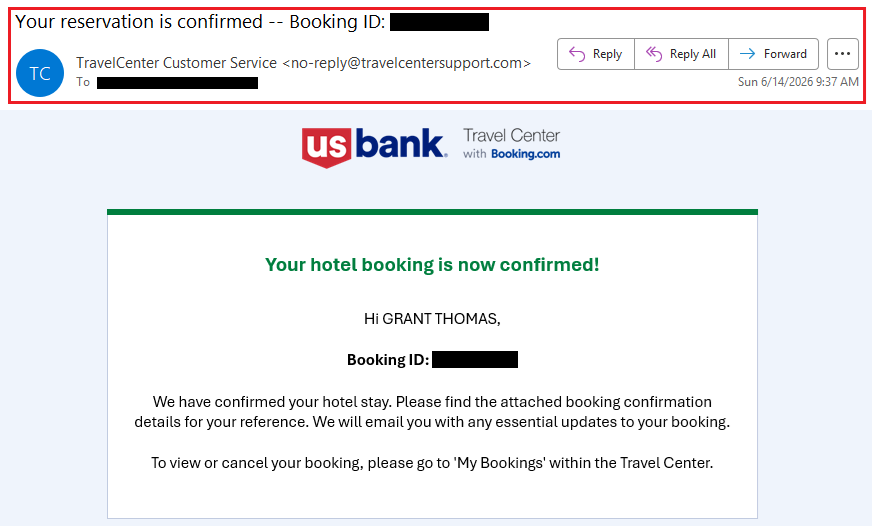

The efficiency of the US Bank Altitude Reserve’s travel credit system can be traced through a specific chronological sequence. On Sunday, June 14, the cardholder initiated a reservation for a two-night stay. The total expenditure of $448 was processed as a prepaid transaction through the US Bank Travel Center. Following the booking, the cardholder received immediate electronic confirmation, and the transaction appeared as a pending charge on the credit card statement.

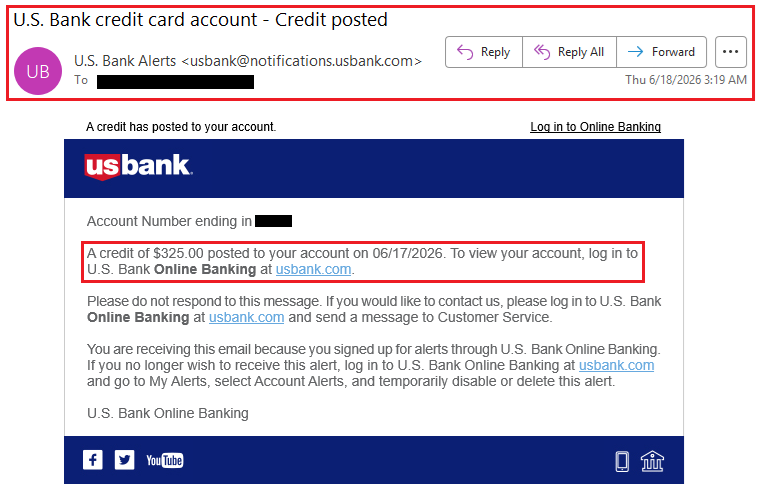

By Thursday, June 18, the US Bank automated system identified the transaction as a qualifying travel expense under the updated terms of the Altitude Reserve program. An electronic notification was dispatched to the cardholder confirming the application of the $325 credit. Upon reviewing the online account activity, both the original $448 debit and the subsequent $325 credit were visible, resulting in a net out-of-pocket expense of $123 for the two-night stay. This four-day turnaround reflects a highly optimized reconciliation process, which is a critical factor for cardholders managing their cash flow and annual benefit windows.

Technical Analysis of Reward Multipliers and Point Accrual

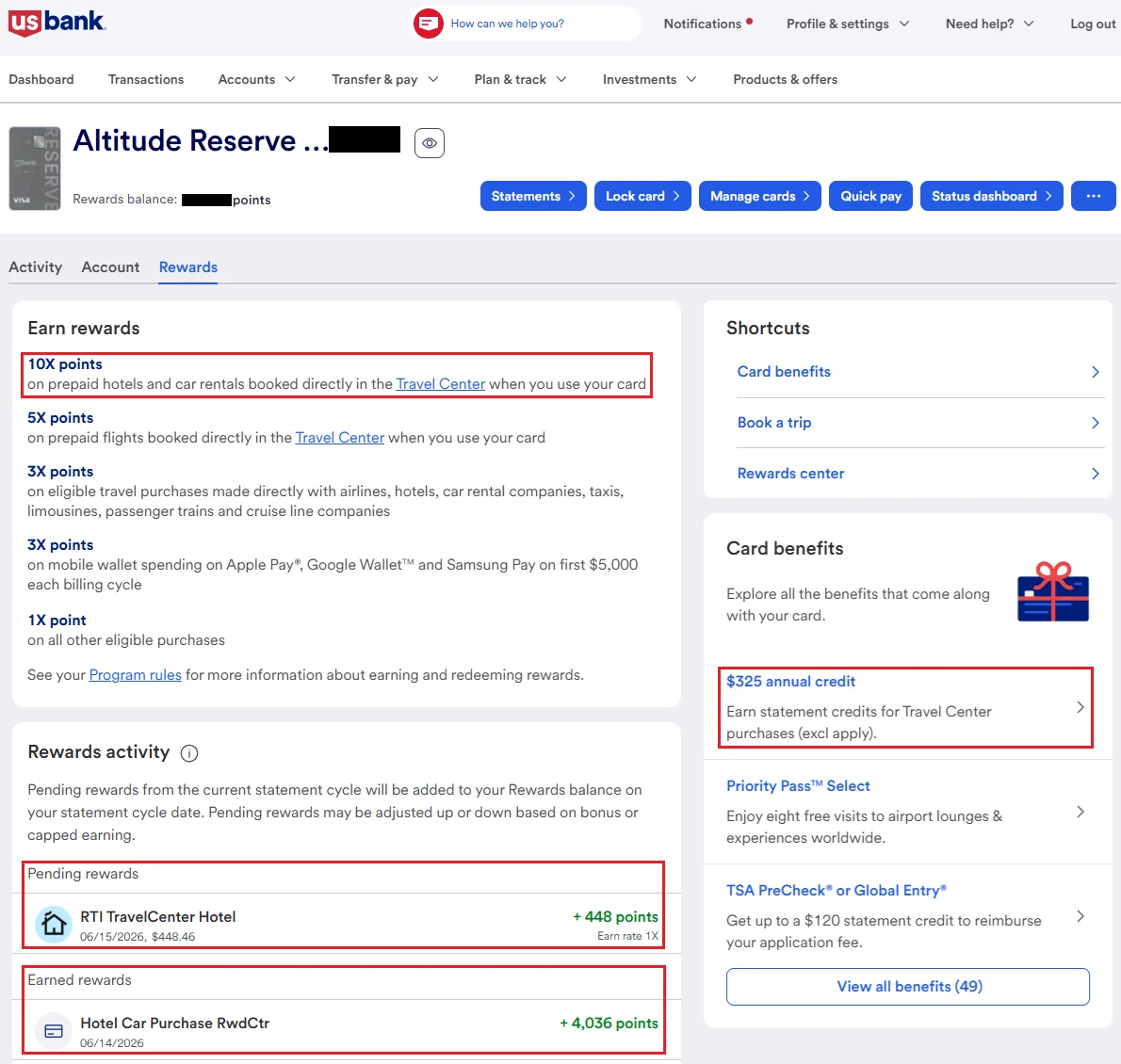

One of the more nuanced aspects of the US Bank Travel Center experience is the accelerated reward earning potential on prepaid hotel stays. According to the card’s current rewards schedule, prepaid hotel reservations and car rentals booked through the portal earn 10 points per dollar spent. However, a detailed analysis of the transaction data reveals that this 10x multiplier is applied specifically to the pre-tax portion of the reservation.

In the case study of the $448 booking, the rewards posted almost immediately to the account’s rewards tab. Interestingly, observers noted a dual-entry system in the pending rewards phase. While the 10x points for the base rate were credited quickly, the full transaction amount initially appeared at the standard 1 point per dollar rate in the pending ledger. This suggests a multi-layered verification system where the bank’s software first acknowledges the base spend and then applies the "bonus" points once the transaction clears the merchant’s processing period. For high-frequency travelers, this 10x earning rate represents a significant return on investment, often exceeding the value offered by competitors’ portals, provided the user is comfortable with the limitations of third-party bookings.

Comparative Landscape: US Bank vs. Peer Institutions

The shift toward portal-based credits is not unique to US Bank. The premium credit card market has seen a general migration toward "walled garden" travel ecosystems. To understand the value proposition of the Altitude Reserve, it is necessary to compare it with other major players:

- Capital One Venture X: This card offers a $300 annual travel credit that is strictly limited to the Capital One Travel portal. While similar to the US Bank model, Capital One provides a price-match guarantee, which mitigates some of the risks associated with portal pricing discrepancies.

- Chase Sapphire Reserve: Chase remains an outlier by offering a $300 travel credit that applies automatically to almost any travel-related purchase, from tolls and parking to airfare and hotels booked directly. This flexibility is often cited as the gold standard for travel credits.

- Citi Strata Elite: Formerly associated with the Prestige or Premier lines, Citi’s hotel benefit (often $100 off a $500+ stay or similar variations) generally requires booking through the Citi Travel portal.

- American Express Platinum: Amex offers a $200 hotel credit, but it is restricted to "Fine Hotels + Resorts" or "The Hotel Collection" bookings made via American Express Travel, which typically cater to the luxury segment.

The US Bank Altitude Reserve’s $325 credit is notably higher than many of its peers, and the inclusion of dining in the credit’s eligibility (though not the focus of this specific portal-based hotel booking) adds a layer of versatility. However, the requirement to use the US Bank Travel Center for hotel-specific redemptions aligns the card more closely with the Capital One Venture X model than the Chase Sapphire Reserve model.

Strategic "Stacking" of Annual Credits

Experienced travelers often engage in a strategy known as "benefit stacking" to minimize the cost of extended trips. This involves distributing a single multi-night itinerary across several different credit card accounts to maximize the utility of various annual credits. In the broader context of the trip mentioned in the source data, a six-night stay was strategically divided into three two-night segments:

- Segment 1: Two nights funded by the US Bank Altitude Reserve $325 credit.

- Segment 2: Two nights funded by the Capital One Venture X $300 credit.

- Segment 3: Two nights funded by the Citi Strata Elite $300 hotel benefit.

This exercise in identifies the most cost-effective hotel night combinations. By isolating the most expensive nights for the cards with the largest credits, or using the portals where the points multipliers are highest, cardholders can effectively neutralize the cost of high-end accommodations. This behavior indicates a sophisticated consumer base that views annual fees not as costs, but as prepayments for travel vouchers that must be strategically deployed.

Industry Implications and the Future of Travel Portals

The move by US Bank to direct travel credit utilization through its own portal is indicative of a broader shift in the financial services industry. Banks are increasingly acting as travel intermediaries for several strategic reasons. First, by directing spend through their own portals, banks capture the commissions that would otherwise go to Online Travel Agencies (OTAs) like Expedia or Booking.com. Second, it allows banks to collect more granular data on customer travel patterns, which can be used to tailor future marketing offers.

From a consumer perspective, the transition is a double-edged sword. While the 10x point multipliers are lucrative, booking through a portal often means forgoing elite status benefits and stay credits within hotel loyalty programs like Marriott Bonvoy, Hilton Honors, or World of Hyatt. Most major hotel chains do not recognize elite status on "third-party" bookings, which includes bank portals. Therefore, the decision to use the US Bank Travel Center involves a trade-off: the immediate financial gain of the $325 credit and 10x points versus the long-term value of hotel-specific loyalty perks.

Conclusion and Outlook

The documented experience with the US Bank Altitude Reserve confirms that while the method of redemption has changed, the efficiency of the credit’s delivery remains high. The four-day turnaround from booking to credit posting suggests a robust technological infrastructure capable of handling high volumes of automated reimbursements.

As the "portal war" between US Bank, Chase, Amex, and Capital One intensifies, consumers can expect to see more aggressive point multipliers—like the 10x offered by US Bank—as an incentive to move away from direct bookings. For the savvy traveler, the key to maximizing value lies in understanding these technical nuances, monitoring the speed of credit postings, and strategically stacking benefits across multiple platforms to ensure that premium annual fees are fully recouped through tangible travel savings. The US Bank Altitude Reserve remains a potent tool in this arsenal, provided the cardholder is willing to navigate the requirements of the US Bank Travel Center.