UBS, the global wealth management powerhouse, has historically maintained a discreet and unconventional approach to its proprietary credit card lineup. Unlike mainstream issuers such as Chase, American Express, or Citi, which frequently leverage aggressive marketing and lucrative sign-up bonuses to capture market share, UBS has traditionally treated its credit cards as quiet utility tools for its existing high-net-worth (HNW) clientele. For years, these cards were notable for their lack of welcome offers, a requirement for significant assets under management or high income for approval, and a strictly analog application process that requires a telephone call rather than a digital form.

In a significant strategic pivot that signals a new appetite for client acquisition and engagement, UBS has introduced substantial welcome offers across its consumer and business credit card suites. These offers, available on both the Visa Infinite and Visa Signature tiers, represent some of the most competitive point-based incentives currently available in the premium financial services sector. Effective immediately and scheduled to remain available through June 30, 2026, these incentives aim to attract affluent spenders who prioritize bespoke service and high-value travel redemptions over the mass-market appeal of traditional rewards cards.

A Detailed Breakdown of the New Welcome Incentives

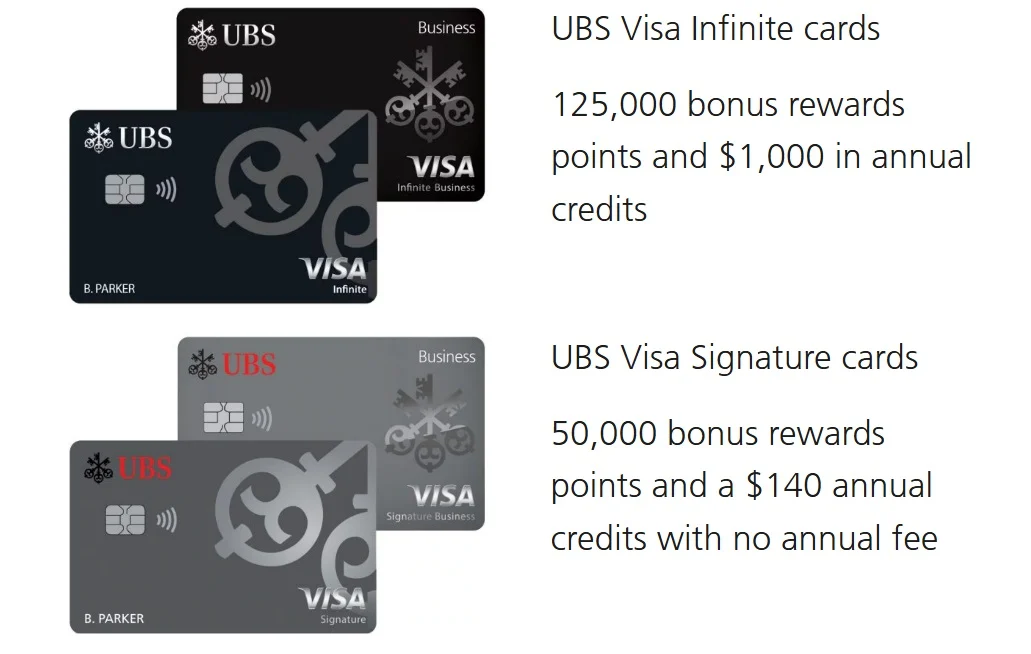

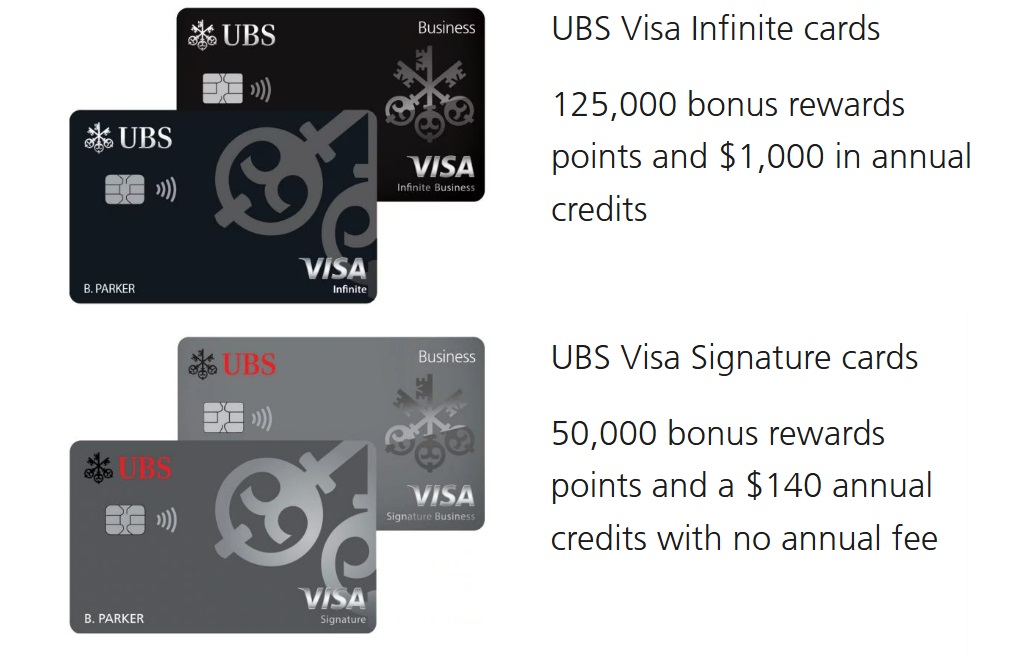

The centerpiece of this update is the 125,000-point welcome offer for the UBS Visa Infinite and the UBS Visa Infinite Business cards. To qualify for this bonus, new cardholders must reach a spending threshold of $6,000 within the first three months of account opening. Given that UBS points can be redeemed at a baseline value of one cent per point, this offer carries a minimum cash-equivalent value of $1,250. However, when utilized through UBS’s specialized travel redemption pathways, the value can appreciate significantly.

Simultaneously, UBS has introduced a 50,000-point offer for its no-annual-fee Visa Signature and Visa Signature Business cards. These cards also require a $6,000 spend within the first three months. While the Signature cards lack the robust travel protections and luxury perks of the Infinite tier, a $500 minimum value on a card with no annual fee is an anomaly in the current market, where no-fee cards typically offer bonuses in the $150 to $200 range.

The introduction of these offers marks a clear departure from the "no-bonus" era of UBS cards. Historically, the value proposition of a UBS card was found in its ongoing benefits and its integration into the broader UBS financial ecosystem. By adding a front-end incentive, UBS is positioning itself to compete directly with the "Big Three" premium cards: the JPMorgan Chase Sapphire Reserve, the American Express Platinum Card, and the Capital One Venture X.

The Economics of UBS My Rewards: Redemption Math and Strategy

One of the most complex aspects of the UBS credit card portfolio is the proprietary "My Rewards" system. Unlike many competitors that offer transfer partners to various airlines and hotels, UBS utilizes a hybrid redemption model that rewards strategic booking.

The baseline redemption rate is a standard 1% (1 cent per point). However, UBS offers two fixed-rate flight redemption options that can significantly elevate the value of the welcome bonus:

- The 25,000-Point Redemption: Cardholders can redeem 25,000 points for a flight costing up to $350. If utilized for a flight priced exactly at $350, the value increases to 1.4 cents per point.

- The 50,000-Point Redemption: Cardholders can redeem 50,000 points for a flight costing up to $900. If maximized, this results in a value of 1.8 cents per point.

For flights exceeding these price caps, UBS employs a "blended" redemption model. For example, if a traveler books a $500 flight, they would use 25,000 points to cover the first $350 of the fare. The remaining $150 would be covered at the standard 1-cent-per-point rate, requiring an additional 15,000 points. The total cost of 40,000 points for a $500 flight results in an effective value of 1.25 cents per point.

Under this math, the 125,000-point welcome offer on the Visa Infinite card could potentially be worth as much as $2,250 if used for two $900 flights (100,000 points) and $250 in other travel or statement credits. This high ceiling for value makes the card particularly attractive to domestic travelers who frequently book mid-to-high-priced economy or regional first-class fares.

Premium Benefits and the High-Net-Worth Barrier

The UBS Visa Infinite cards carry a $650 annual fee, placing them at the upper echelon of premium credit products. However, the card’s benefit structure is designed to provide a "net-positive" experience for the frequent traveler. A primary feature is the $500 annual airline fee credit. This credit applies to a selected domestic airline and covers ancillary charges such as baggage fees, seat upgrades, and in-flight refreshments. Because this credit is issued on a calendar-year basis, a new cardholder could potentially claim $500 in credits in 2024, another $500 in 2025, and a third $500 in early 2026, all within the first two years of membership.

Beyond the airline credit, the UBS Visa Infinite offers a Priority Pass Select membership that remains one of the most robust in the industry. While many issuers have stripped restaurant access from their Priority Pass benefits, the UBS version currently retains it, along with unlimited guesting privileges. This distinction is vital for travelers who frequent airports with high-quality Priority Pass-affiliated dining options rather than traditional lounges.

Additional benefits include:

- Global Entry or TSA PreCheck Credit: Up to $120 every four years.

- GigSky Data Roaming: A complimentary 5GB, 30-day cellular data plan annually, usable in over 125 countries.

- $500 High-Spend Bonus: Cardholders who spend $25,000 in a calendar year receive an additional $500 credit applicable toward Amazon Prime, restaurant purchases, or airport lounge fees.

- Primary Rental Car Insurance: Coverage that takes precedence over personal insurance for both domestic and international rentals.

Despite these riches, the barrier to entry remains high. UBS does not offer an online application for these cards; prospective clients must call 866-827-8472 to initiate the process. Furthermore, the cards are intended for individuals who already have a relationship with UBS Wealth Management or who meet the internal criteria for high-net-worth status. This gatekeeping ensures that the card remains an exclusive tool for a specific demographic rather than a mass-market product.

Comparative Chronology and Market Context

To understand the significance of these offers, one must look at the timeline of the premium credit card market over the last decade. Following the 2016 launch of the Chase Sapphire Reserve, which featured a 100,000-point bonus, the industry entered an "arms race" of sign-up incentives. UBS, however, remained largely on the sidelines, maintaining a "service-first" model that relied on the prestige of the UBS brand rather than transactional incentives.

The current shift suggests that even the most exclusive wealth management firms are feeling the pressure of "loyalty dilution." As younger generations of high-net-worth individuals enter the market, they are proving to be more "reward-literate" than their predecessors. They are less likely to carry a card simply because it bears the name of their private bank and more likely to carry the card that offers the best return on spend.

The expiration date of June 30, 2026, is also noteworthy. Most credit card offers are "limited time" and expire within weeks or months. By setting a two-year window, UBS is signaling that this is not a desperate push for numbers, but a long-term recalibration of their client acquisition strategy.

Impact on the Wealth Management Landscape

Industry analysts view this move as a component of "relationship banking." By embedding a high-value credit card into a client’s daily life, UBS increases the "stickiness" of the relationship. A client who uses a UBS Visa Infinite for their daily business expenses and travel is less likely to move their investment portfolio to a competitor.

The "Business" versions of these cards are particularly potent in this regard. The UBS Visa Infinite Business card offers 3x points on air travel and hotel stays and 2x points on common business expenses like office supplies and advertising. For a business owner with several million dollars in annual spend, the rewards accumulation, combined with the 1.8-cent-per-point redemption potential, creates a compelling financial argument for consolidating spending on the UBS platform.

Conclusion and Final Analysis

The new welcome offers from UBS represent a rare opportunity for affluent consumers to extract significant value from a prestigious issuer. While the $650 annual fee for the Infinite tier is high, the $500 airline credit and the 125,000-point bonus (worth up to $2,250 in flights) provide an overwhelming mathematical justification for the card in the first year.

For the no-annual-fee Signature cards, the 50,000-point offer is a market-leading incentive that brings UBS into the conversation for "best-in-class" no-fee rewards. However, the requirement to apply via phone and the focus on high-net-worth individuals will keep these cards out of reach for the general public. For those who qualify, the window of opportunity is now open, providing a rare bridge between the world of private banking and the lucrative world of high-end travel rewards. As the June 2026 deadline approaches, it remains to be seen if UBS will make these offers a permanent fixture or return to the quiet, bonus-free exclusivity that defined its past.