The financial landscape of travel often hinges on the reliability of ancillary benefits provided by premium credit cards, particularly regarding Auto Rental Collision Damage Waivers (CDW). A recent incident involving a rental vehicle from Hertz Global Holdings, Inc., operated by members of the travel media outlet Frequent Miler, serves as a significant case study in the logistical and administrative realities of these insurance products. While traveling on a highway toward Colorado Springs for a professional consultation with the blog hosting entity Boarding Area, the team’s rented minivan sustained a cracked windshield from a rock strike. This event initiated a series of administrative actions that highlight the critical distinctions between various Chase-branded financial products, the efficacy of primary insurance coverage, and the current state of rental car damage recovery protocols.

The Operational Context and the Insurance Experiment

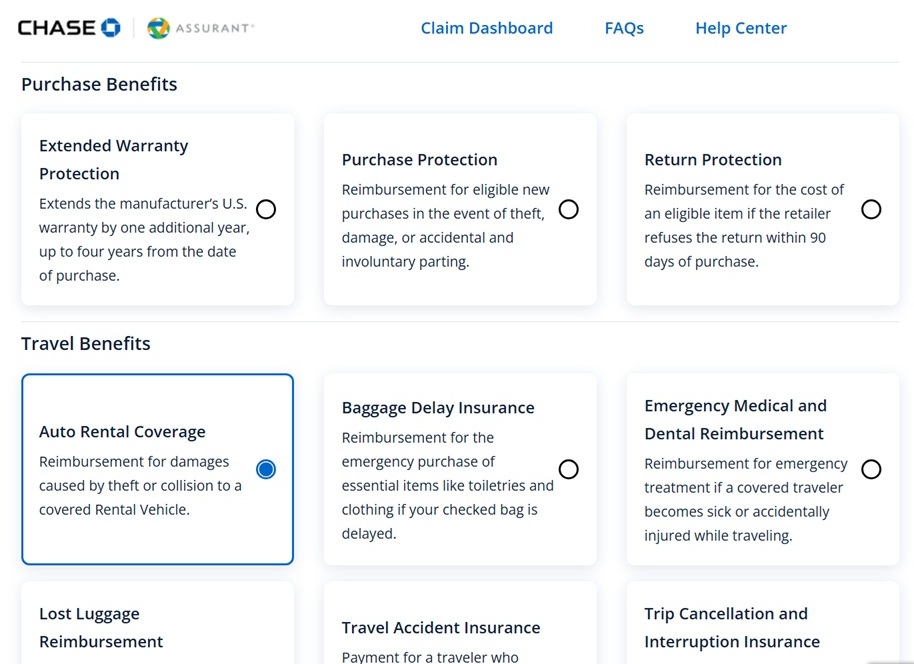

The incident occurred during a transit from Denver to Colorado Springs, a route frequently susceptible to road debris. Despite the visible damage to the windshield, the vehicle remained operational, allowing the team to proceed to their scheduled working meetings. The circumstances provided a unique opportunity to test the primary rental insurance coverage of the Ink Business Preferred® Credit Card, a product marketed by JPMorgan Chase.

The Ink Business Preferred® card is frequently cited in the travel industry for its robust 3X reward structure on travel purchases. However, its Auto Rental Collision Damage Waiver carries a specific regulatory caveat: within the United States, coverage is primary only if the rental is for "legitimate business purposes." For personal travel, the coverage typically reverts to secondary, meaning the claimant must first exhaust their personal auto insurance policy before the credit card benefit compensates for the remaining balance. Because the Frequent Miler team was traveling for a business meeting, the situation represented a controlled environment to observe how Chase and its third-party underwriters verify commercial intent.

However, a breakdown in rental agency synchronization altered the parameters of this experiment. Despite the claimant’s intent to use the Ink Business Preferred® card, Hertz’s internal systems defaulted to the payment method on the user’s gold member profile—the Chase Sapphire Reserve®. While the Sapphire Reserve® also offers primary coverage, it does so for both personal and business travel without the same restrictive clauses found on the Ink Business Preferred®. This shift in payment methods underscores a common pitfall in rental logistics: the "default card" override, which can inadvertently shift a traveler’s insurance strategy.

Chronology of the Damage Recovery Process

The timeline for resolving a rental car damage claim is rarely instantaneous, involving a multi-stage process of reporting, estimation, and adjudication. In this instance, the timeline stretched over approximately six weeks from the date of the incident to the final reimbursement.

The Vehicle Return and Incident Reporting

The vehicle was returned to the Hertz facility at the conclusion of the rental period. Unlike standard returns, which are often processed in seconds via mobile handhelds, a damage report requires a formal "Incident Report." This process was described as labor-intensive due to technical instabilities in the rental agency’s proprietary software. The attendant used a tablet-based application to document the damage, take photographic evidence, and collect the driver’s personal information. The process was marred by multiple system crashes, necessitating repetitive data entry.

A critical decision point occurred when the app queried whether the rental agency should pursue the claimant’s personal insurance or if the claimant would handle the recovery independently. In this case, the claimant opted for the former, mistakenly providing the credit card’s benefit phone number as the primary insurance provider. While this led to a minor administrative delay, Hertz eventually bypassed the direct-to-insurance route and sent the final bill directly to the customer, allowing for a standard claim submission.

The Financial Assessment

It took nearly four weeks for Hertz Central Recovery to issue a formal repair estimate. The total invoice amounted to $746.92. This figure is consistent with modern automotive repair costs; while a simple glass replacement might have cost significantly less in previous decades, contemporary vehicles often house Advanced Driver Assistance Systems (ADAS) behind the windshield. Replacing the glass frequently necessitates the recalibration of cameras and sensors, which significantly inflates labor and equipment costs.

The Claim Adjudication

Upon receiving the PDF of the vehicle incident report and the final bill, the claimant initiated a case through the Chase Card Benefits portal (chasecardbenefits.com). The digital interface, managed by third-party administrators, allows for the electronic submission of required documentation, including:

- The original rental agreement.

- The final rental receipt showing the full payment on the eligible card.

- The internal incident report from the rental agency.

- The itemized repair estimate or final bill.

- A copy of the credit card statement reflecting the rental charge.

The efficiency of this digital workflow was notable. Once the documentation was submitted, the claim was reviewed and approved within six business days. The full reimbursement of $746.92 was deposited into the claimant’s bank account two days after approval.

Comparative Analysis: Primary vs. Secondary Coverage

The distinction between primary and secondary coverage is the most significant factor for travelers when choosing a payment method for vehicle rentals.

Primary Coverage: As seen in this case with the Chase Sapphire Reserve®, primary coverage pays out before any other insurance policy. This is highly advantageous for the consumer because it prevents the incident from being reported to their personal auto insurance provider, thereby avoiding potential premium increases or "points" on their driving record.

Secondary Coverage: Most standard credit cards offer secondary coverage. In the event of a $746.92 claim, the traveler would first have to file a claim with their personal insurance (e.g., Geico, State Farm). The traveler would be responsible for their deductible (often $500 or $1,000), and the credit card would only cover the portion the personal insurance did not pay. Furthermore, the claim would be recorded on the individual’s Comprehensive Loss Underwriting Exchange (CLUE) report.

The $746.92 recovery in this case illustrates the high value of the Sapphire Reserve’s $550 annual fee. By successfully navigating the primary claim, the traveler saved the equivalent of several years of the card’s net cost while protecting their personal insurance rating.

Institutional Responses and Industry Background

Hertz’s handling of the incident reflects broader industry trends in damage recovery. The company has moved toward centralized recovery units to standardize how they bill for "loss of use" (revenue lost while the car is in the shop) and administrative fees. While this case focused on the direct repair cost, rental agencies often attempt to recoup these additional expenses, which are also typically covered by Chase’s primary insurance.

The mention of "avoiding jail" during the team’s initial reaction refers to a well-publicized controversy involving Hertz. In late 2022, Hertz agreed to pay approximately $168 million to settle 364 claims from customers who were falsely arrested after the company reported vehicles as stolen due to internal clerical errors. While the Frequent Miler team’s joke was lighthearted, it highlights a period of significant reputational friction for the rental giant regarding its administrative accuracy.

Broader Implications for Travelers

The successful resolution of this claim provides several key takeaways for both business and leisure travelers:

- Profile Management: Travelers must ensure that their rental car loyalty profiles (Hertz Gold Plus Rewards, Avis Preferred, etc.) are updated with the specific card they intend to use for insurance purposes. The automated systems at checkout will almost always prioritize the profile’s default card over a one-time reservation entry.

- Documentation is Paramount: The speed of the Chase claim (six days) was largely due to the claimant having a complete PDF "paper trail." Travelers should never leave a rental lot after an incident without a signed copy of the incident report and photos of the damage.

- The Value of Premium Glass: As vehicles become more technologically advanced, even "minor" damage like a windshield crack will likely exceed the $500 mark. This makes primary credit card insurance more valuable than ever, as it covers the full cost of high-tech glass and sensor recalibration.

- Digital Claims Portals: The transition from phone-based claims to dedicated web portals like chasecardbenefits.com has significantly reduced the friction of the reimbursement process. The ability to track a claim status in real-time provides a level of transparency that was previously absent in the insurance industry.

In conclusion, while the rock strike on the highway was an unforeseen nuisance, the subsequent administrative process validated the utility of premium credit card benefits. The $746.92 reimbursement serves as a factual endorsement of maintaining a card with primary rental coverage, provided the traveler understands the nuances of their card’s specific policy requirements and remains diligent in their documentation. The failure of the "business purpose" experiment with the Ink Business Preferred® remains a cautionary tale about the power of default settings in the automated travel economy.