The landscape of consumer finance has increasingly shifted toward incentivized spending, with the pursuit of credit card welcome bonuses becoming a primary driver for travelers and points enthusiasts seeking to accumulate significant caches of rewards. Central to this pursuit is the "minimum spend requirement," a contractual obligation that dictates a specific amount of capital must be charged to a new credit card within a predetermined window of time to trigger a promotional payout of points, miles, or cash back. While these offers can provide thousands of dollars in value, navigating the technical nuances of spend timelines, eligible transactions, and institutional quirks is essential for financial success.

The Structural Framework of Modern Welcome Offers

In the competitive credit card market, financial institutions utilize welcome bonuses as a primary tool for customer acquisition. These bonuses are rarely awarded immediately upon approval; instead, they are contingent upon the cardholder demonstrating active use of the line of credit. The minimum spend requirement (MSR) typically consists of two variables: the total dollar amount required and the duration of the eligibility period.

Industry standards for these requirements vary significantly based on the card’s target demographic. Entry-level cards may require as little as $500 to $1,000 in spend over three months, while premium travel cards often demand $4,000 to $6,000. High-end business cards represent the upper echelon of this spectrum, frequently requiring $15,000 to $30,000 in expenditures within a three-to-six-month window.

Occasionally, issuers deviate from this model. For instance, certain retail-branded cards or specialized products like the Bilt Mastercard have historically offered bonuses upon approval or after a single purchase. However, as banks seek to ensure long-term profitability and "top-of-wallet" status, high-threshold spending requirements have become the prevailing industry norm.

The Evolution and Chronology of Spending Incentives

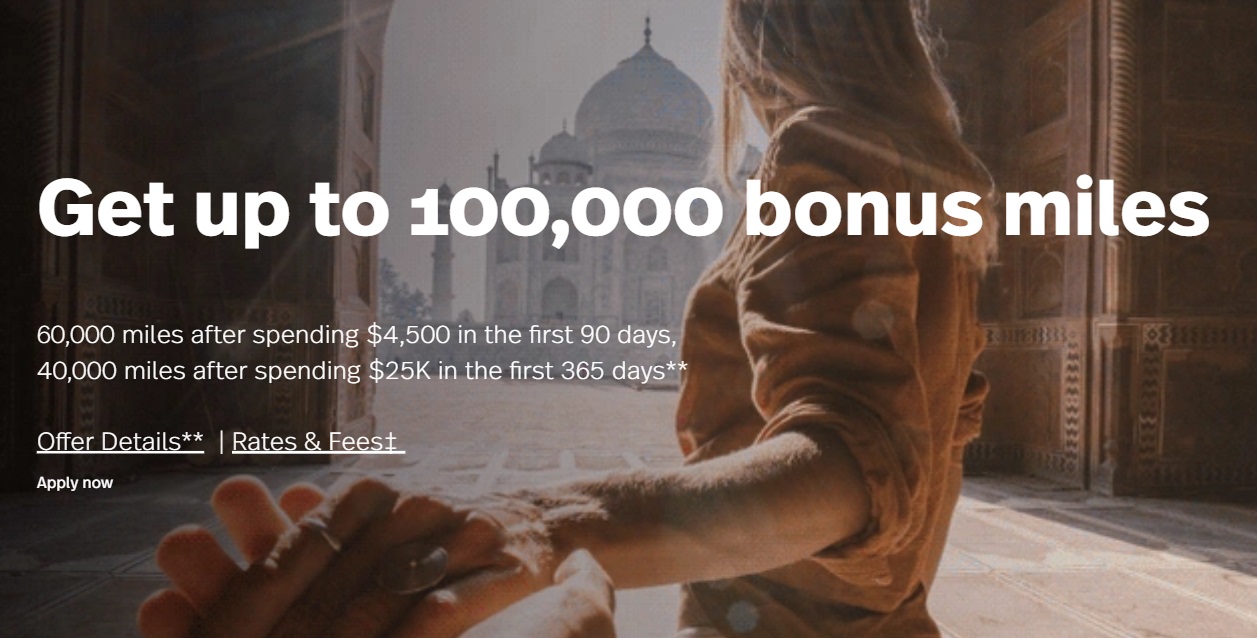

The strategy of utilizing welcome offers has evolved from a niche hobby into a mainstream financial tactic. In the early 2010s, requirements were generally lower and timelines more flexible. The 2016 launch of the Chase Sapphire Reserve, which offered 100,000 points for a $4,000 spend, marked a turning point in consumer awareness and bank aggression. Since then, issuers have introduced "tiered" spending requirements to encourage sustained usage over a longer duration.

Tiered structures operate on a cumulative basis. A common example in the current market involves a two-part bonus: a cardholder might earn 60,000 points after spending $4,000 in the first three months, and an additional 40,000 points after reaching a total of $10,000 in spend within six months. Financial analysts observe that this structure serves a dual purpose: it lowers the barrier to entry for the initial bonus while providing a secondary incentive that prevents the "sock-drawering" of a card—the practice of stopping all spend once a bonus is earned.

Critical Timing: The Application Date vs. The Activation Date

One of the most frequent pitfalls for new cardholders is a misunderstanding of when the spending clock begins. For the vast majority of issuers, including American Express, Chase, and Citi, the countdown begins on the date of application approval, not the date the physical card is received or activated.

This distinction is critical because the logistics of card delivery can consume a significant portion of the eligibility window. While some premium cards offer expedited shipping or instant digital card numbers for use in mobile wallets, standard delivery can take seven to ten business days. If an application is placed under "pending review," the time spent in manual underwriting further compresses the window. For a card with a 90-day requirement, a two-week delay in receiving the card effectively reduces the cardholder’s daily spending capacity by nearly 15%.

Furthermore, there is a legalistic distinction between "90 days" and "three months." In a calendar year, 90 days is almost always shorter than three full months. For example, an application approved on June 1st with a 90-day window would expire on August 30th, whereas a three-month window would extend to September 1st. Missing the deadline by even 24 hours generally results in a total forfeiture of the bonus, with banks rarely granting extensions.

Data-Driven Tracking and Verification Strategies

To mitigate the risk of missing a bonus, sophisticated consumers have adopted rigorous tracking methods. While major issuers like American Express now provide digital "progress bars" within their mobile apps to track spend in real-time, these tools are not universal.

Industry experts recommend three primary layers of verification:

- Visual Documentation: Taking screenshots of the specific offer terms during the application process. This provides evidence in the event of a "zombie offer" or a technical glitch where the bank’s internal system does not automatically attach the promotion to the account.

- Manual Accounting: Utilizing spreadsheets to record the approval date, the exact deadline, and the net spend.

- The "Buffer" Principle: Aiming to exceed the minimum spend by several hundred dollars. This accounts for the possibility of returned items or disputed charges which, if they occur after the deadline, can lead to a retroactive "clawback" of the bonus points by the issuer.

Identifying Ineligible Transactions and Institutional Quirks

A common misconception is that all charges appearing on a billing statement count toward the minimum spend requirement. In reality, several categories of outflows are strictly excluded:

- Annual Fees: The cost of carrying the card itself does not count toward the requirement.

- Cash Equivalents: Cash advances, balance transfers, and the purchase of money orders or traveler’s checks are excluded to prevent "manufactured spending."

- Interest and Late Fees: Any financing charges applied by the bank are ineligible.

Institutional policies also introduce unique hurdles. For instance, US Bank has historically maintained a policy where only the primary cardholder’s spending counts toward the bonus; purchases made by authorized users may earn standard rewards but fail to move the needle on the welcome offer. Similarly, certain issuers have begun excluding "rent-like" or "tax-like" payments from bonus eligibility to ensure the spend reflects organic consumer behavior rather than large, one-off financial obligations.

Strategic Financial Planning for High-Threshold Requirements

For cardholders facing substantial spend requirements, such as those found on business-grade products, "organic" daily spending on groceries and fuel may be insufficient. This necessitates a "plan ahead" strategy. Large, infrequent expenses—such as quarterly estimated tax payments, insurance premiums, tuition, or home renovation deposits—provide an ideal mechanism for meeting requirements without inflating one’s lifestyle.

However, financial advisors warn against "spending for the sake of the bonus." If a consumer spends $5,000 on unnecessary luxury goods to earn a $750 travel credit, the net financial result is a loss of $4,250. The most successful practitioners of this strategy align their card applications with pre-existing, mandatory expenses.

Broader Impact and Market Implications

The prevalence of minimum spend requirements has broader implications for the credit industry and consumer behavior. From a macroeconomic perspective, these incentives drive high transaction volumes, which in turn generate interchange fees for banks and payment networks like Visa and Mastercard.

For the consumer, the impact is two-fold. On the positive side, it allows for "subsidized" travel and high-value rewards that would otherwise be unattainable. On the negative side, the pressure to meet a spending deadline can lead to credit card debt if the cardholder cannot pay the balance in full by the end of the billing cycle. The interest rates on rewards cards are notoriously high, often exceeding 20-25%. If a cardholder carries a balance while chasing a bonus, the interest charges will almost certainly outpace the value of the points earned, negating the benefit of the welcome offer.

Conclusion: The Professional Approach to Rewards

Minimum spend requirements are the "cost of admission" for the lucrative world of credit card rewards. Achieving success requires more than just high spending; it demands an analytical approach to timing, a clear understanding of bank-specific exclusions, and a disciplined tracking system. By treating a credit card application as a strategic financial project rather than a simple transaction, consumers can maximize their rewards while maintaining the integrity of their long-term financial health. As the industry continues to evolve with more complex tiered offers and stricter "anti-gaming" rules, the importance of meticulous planning and data-driven tracking will only increase.