The global hospitality sector has undergone a profound transformation over the last decade, transitioning from a fragmented market of regional players into a consolidated industry dominated by a handful of multinational behemoths. At the center of this evolution is the metric of market capitalization, which serves as the ultimate barometer for investor confidence, brand equity, and long-term scalability. Recent data indicates that while the hierarchy of the world’s largest hotel chains remains relatively stable, the valuation gaps between these entities are shifting, reflecting broader economic trends and individual corporate strategies. As of the second quarter of 2024, Marriott International and Hilton Worldwide Holdings continue to lead the pack, maintaining a significant lead over competitors such as Hyatt Hotels Corporation, InterContinental Hotels Group (IHG), and Accor.

The Valuation Hierarchy: Defining the Industry Leaders

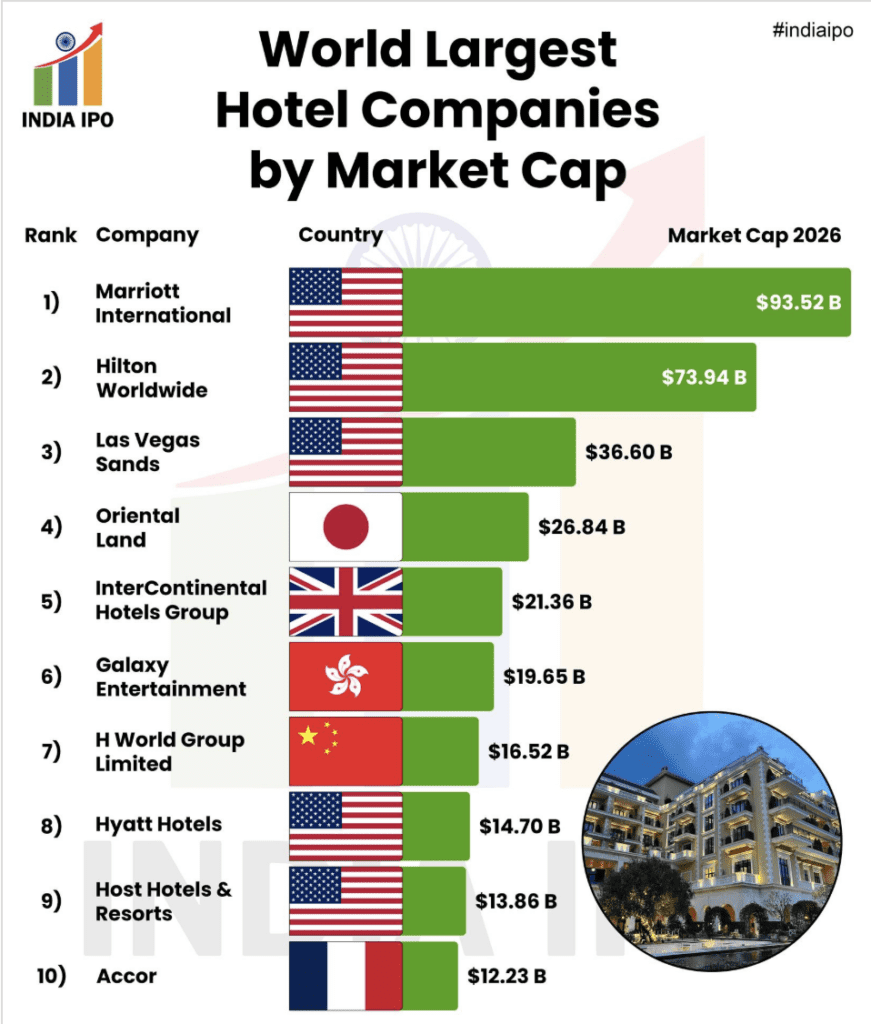

In the current financial climate, Marriott International stands as the preeminent force in the hospitality world. With a market capitalization frequently hovering between $70 billion and $80 billion, Marriott’s valuation is nearly six to seven times that of Hyatt Hotels Corporation. This discrepancy is a point of frequent discussion among industry analysts. While anecdotal evidence in travel circles previously suggested a "10X gap" between the industry titans and Hyatt, contemporary market data shows a more nuanced reality. The current ratio of approximately 6.36X suggests that while Hyatt remains a smaller player in terms of sheer volume and market value, it has maintained a resilient position relative to the aggressive growth of the "Big Two."

Hilton Worldwide Holdings occupies the second position, with a market capitalization often exceeding $50 billion. The rivalry between Marriott and Hilton defines much of the modern hospitality strategy, as both companies race to expand their global footprints through "asset-light" business models. Following these leaders are several major international players, including the InterContinental Hotels Group (IHG), based in the United Kingdom, and the Indian Hotels Company Limited (IHCL), which operates the prestigious Taj brand. The inclusion of IHCL in the top tier of global hotel valuations highlights the surging importance of the Indian domestic market and the growing international influence of South Asian hospitality conglomerates.

A Chronology of Consolidation and Growth

The current market landscape is the result of a series of strategic maneuvers that began in earnest following the 2008 financial crisis. The most significant turning point occurred in 2016, when Marriott International acquired Starwood Hotels & Resorts Worldwide in a deal valued at approximately $13 billion. This merger created the world’s largest hotel company, bringing together iconic brands like Ritz-Carlton and St. Regis with Sheraton and Westin. The acquisition was a catalyst for the "arms race" of loyalty programs, as Marriott sought to integrate Starwood Preferred Guest (SPG) into what eventually became Marriott Bonvoy.

Parallel to Marriott’s expansion, Hilton Worldwide underwent a massive structural reorganization. In 2017, Hilton spun off the majority of its real estate business into a separate publicly traded real estate investment trust (REIT) called Park Hotels & Resorts. This move allowed Hilton to become a pure-play management and franchise company, significantly boosting its market valuation by shedding capital-intensive physical assets. This "asset-light" strategy has since become the industry standard, favored by investors for its high margins and lower exposure to real estate market volatility.

Hyatt Hotels Corporation has followed a different trajectory, focusing on "intentional growth" rather than mass-market saturation. In 2021, Hyatt made a major strategic play by acquiring Apple Leisure Group (ALG) for $2.7 billion. This acquisition significantly expanded Hyatt’s presence in the luxury all-inclusive resort space, a segment that has seen explosive demand in the post-pandemic era. This move was a clear signal that Hyatt intended to compete on quality and high-yield segments rather than trying to match the room count of Marriott or Hilton.

Supporting Data: Room Counts and Loyalty Ecosystems

Market capitalization is inextricably linked to the size of a hotel’s "pipeline" and the depth of its loyalty program. Marriott currently manages or franchises over 8,700 properties across 139 countries and territories, totaling more than 1.5 million rooms. Its loyalty program, Marriott Bonvoy, boasts over 200 million members. This massive database of consumers provides a "moat" that protects the company’s valuation, as it allows Marriott to drive direct bookings and reduce its reliance on high-commission third-party Online Travel Agencies (OTAs) like Expedia and Booking.com.

Hilton operates approximately 7,500 properties with over 1.1 million rooms. Its Hilton Honors program, with over 180 million members, is widely cited for its consistency and user-friendly technology. The close competition between Marriott and Hilton is reflected in their stock performance; both companies have seen their share prices reach record highs in 2023 and 2024, driven by a "revenge travel" surge and the recovery of the business travel sector.

In contrast, Hyatt maintains a more boutique footprint with roughly 1,300 properties. While its room count is a fraction of its larger peers, Hyatt’s focus on the upper-upscale and luxury segments allows it to command higher Average Daily Rates (ADR) and Revenue Per Available Room (RevPAR). This high-margin focus is why Hyatt’s market cap, while smaller, remains robust enough to keep it in the top tier of global hospitality firms.

Strategic Shifts and Official Industry Perspectives

Executives across the major chains have recently shifted their public messaging toward "digital transformation" and "lifestyle brands." During recent earnings calls, Marriott CEO Anthony Capuano emphasized the company’s focus on diversifying its portfolio into midscale segments—such as the "StudioRes" brand—to capture a wider demographic of travelers. This indicates that even the largest players see a need to fill gaps in their portfolio to maintain market cap dominance.

Hilton’s CEO, Christopher Nassetta, has frequently spoken about the importance of "organic growth." Unlike Marriott, which grows significantly through large-scale acquisitions, Hilton has historically preferred to launch its own brands, such as Spark and Tempo. This strategy is viewed favorably by investors who prefer the lower risk associated with internal brand development versus the complex integration of multi-billion dollar acquisitions.

From a broader industry perspective, the rise of the Indian Hotels Company Limited (IHCL) signals a shift in where capital is flowing. IHCL’s market capitalization has seen significant appreciation as the Indian economy expands. Analysts suggest that the next decade may see a "multipolar" hospitality market where Asian-based firms challenge the traditional North American and European hegemony in the top ten rankings.

Fact-Based Analysis of Market Implications

The concentration of market value in a few large corporations has several implications for the global economy and the consumer experience. First, the "asset-light" model that drives these high valuations means that the companies themselves own very little real estate. Instead, they sell their brand expertise, reservation systems, and loyalty networks to third-party owners. This shift has turned hotel companies into technology and marketing firms that happen to operate in the physical world.

For investors, the high market caps of Marriott and Hilton represent a "safe haven" within the discretionary spending sector. These companies have demonstrated an ability to maintain pricing power even during inflationary periods. However, the 6.36X valuation gap between Hyatt and Marriott also suggests that there is still room for "mid-sized" giants to thrive by targeting specific niches that the larger chains might overlook due to their scale.

The data also reveals a potential vulnerability: the reliance on loyalty programs. As these programs grow to hundreds of millions of members, "points inflation" becomes a risk. If consumers perceive that their loyalty is not being rewarded with tangible value, the brand equity—and subsequently the market capitalization—of these giants could face downward pressure.

Future Outlook: Sustainability and Digital Integration

Looking ahead, the market capitalization of these hotel chains will increasingly be influenced by their Environmental, Social, and Governance (ESG) performance. Institutional investors are placing higher premiums on companies that can demonstrate a clear path to net-zero emissions. Marriott, Hilton, and Hyatt have all released comprehensive sustainability reports, but the cost of retrofitting thousands of franchised properties to meet modern green standards remains a significant long-term challenge.

Furthermore, the integration of Artificial Intelligence (AI) into the booking and stay experience is expected to be the next frontier for valuation growth. Companies that can successfully use AI to personalize travel experiences and optimize dynamic pricing will likely see their market caps outpace those that are slower to adapt.

In conclusion, the global hotel market is currently defined by a clear hierarchy where Marriott and Hilton reign supreme, yet the competitive landscape remains dynamic. The "narrowing" of the perceived gap between Hyatt and its larger rivals indicates a market that values specialized luxury and lifestyle offerings alongside mass-market scale. As the industry moves further into the 2020s, the battle for market capitalization will be fought not just on the ground with new hotel openings, but in the digital realm through data analytics, loyalty ecosystem expansion, and sustainable business practices.