The recent International Air Transport Association (IATA) Annual General Meeting (AGM) in Rio de Janeiro, Brazil, concluded with a resounding, albeit familiar, chorus of airline frustrations, yet one particular theme dominated the discourse: the increasing leverage of engine and parts manufacturers over airline operations and profitability. While fuel costs traditionally hogged the spotlight, the 79th iteration of this pivotal industry gathering saw airline leaders direct their loudest complaints toward the companies producing the vital components that keep aircraft flying. The consensus among executives was stark: engine makers are unequivocally gaining the upper hand, leaving airlines to contend with escalating costs, prolonged waiting periods for essential maintenance and parts, and a consequential reduction in operational fleets, with seemingly limited recourse. This shift in power dynamics represents a critical challenge for an industry still navigating a complex post-pandemic recovery.

The IATA AGM serves as the airline industry’s premier annual summit, bringing together CEOs, senior executives, and government officials from across the globe. It is a forum for strategic discussions, policy debates, and the setting of industry priorities. Held this year against the vibrant backdrop of Rio, the meeting was anticipated to address key issues such as sustainability, digitalization, and market liberalization. However, beneath these broader strategic objectives, a more immediate and pressing operational crisis emerged as the central talking point, underscoring the delicate interdependence within the aviation ecosystem.

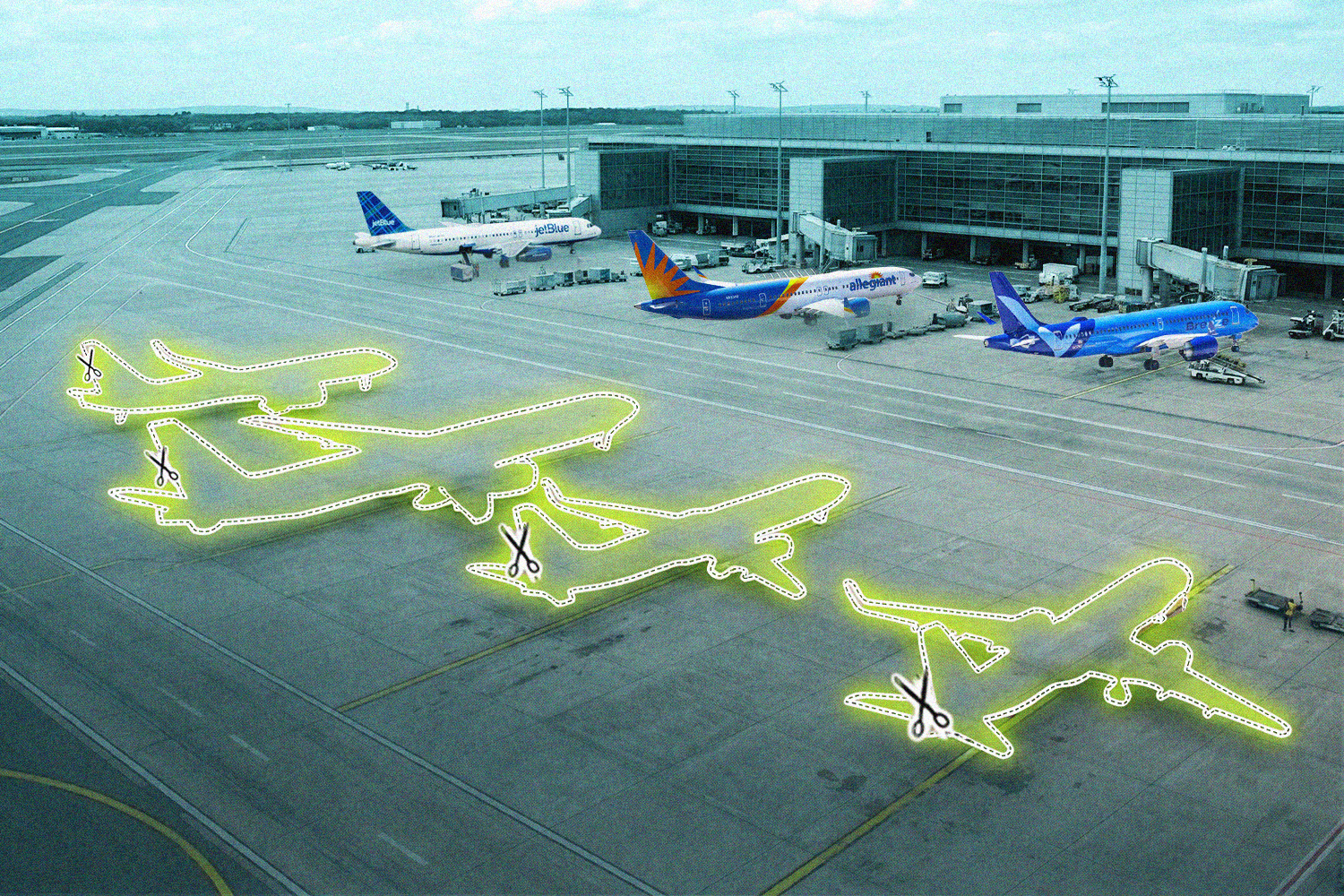

The Core Grievance: Engine and Parts Bottlenecks

The primary source of airline discontent stems from a confluence of factors impacting the availability and maintenance of aircraft engines and other critical components. For years, airlines have operated on tight margins, meticulously planning fleet utilization and maintenance schedules to maximize efficiency. The current environment, however, has thrown these plans into disarray. Grounded aircraft, or "Aircraft on Ground" (AOG) situations, due to a lack of spare parts or prolonged maintenance, are becoming increasingly common and costly.

A significant portion of the frustration is directed at the original equipment manufacturers (OEMs), particularly those producing new-generation engines. Engines like the Pratt & Whitney Geared Turbofan (GTF) powering many Airbus A320neo family aircraft, and the CFM LEAP engines used on both the A320neo and Boeing 737 MAX, have experienced well-documented durability issues and required more frequent maintenance than initially projected. While manufacturers continuously work to address these "teething problems" inherent in new technology, the sheer scale of the global fleet utilizing these engines means that even minor design or material flaws can lead to widespread operational disruptions.

Beyond the engines themselves, a broader scarcity of essential parts—from landing gear components and avionics to interior elements—is exacerbating the problem. The intricate global supply chain for aerospace manufacturing, already fragile after the pandemic, has struggled to rebound to pre-COVID efficiency levels. Raw material shortages, labor scarcity at various production tiers, and logistics bottlenecks have all contributed to extended lead times for parts that once could be acquired relatively quickly.

The Economic Imperative: Why Airlines Are Struggling

The financial implications for airlines are profound. Every aircraft that sits idle due to maintenance or lack of parts represents a significant capital expenditure generating no revenue. Industry analysts estimate that hundreds of aircraft globally are currently grounded for extended periods, directly impacting airline capacity and profitability. For a typical narrow-body aircraft, daily operating costs, even when grounded, can run into tens of thousands of dollars, excluding lost revenue. Over a year, this can amount to millions per aircraft.

Furthermore, the costs associated with maintenance, repair, and overhaul (MRO) have surged. Airlines are not only paying more for parts but also for the specialized labor and facility time required for extensive overhauls. Some estimates suggest MRO costs have increased by 15-25% in the past year alone for certain engine types. This directly impacts airlines’ bottom lines, eroding the hard-won gains from the post-pandemic travel rebound. Given that fuel costs remain volatile, and labor expenses are rising due to widespread shortages, the added burden from MRO and parts delays creates a formidable financial headwind.

The ripple effect extends to fleet planning and network expansion. Airlines that had ambitious growth plans based on new aircraft deliveries are finding their schedules disrupted. Delays in receiving new aircraft from manufacturers, often tied to the same supply chain issues affecting parts, mean that airlines cannot deploy the planned capacity, impacting their ability to meet surging passenger demand and capitalize on new market opportunities.

Voices from Rio: Airline Leaders Speak Out

While specific quotes were often off-the-record or generalized, the sentiment from airline executives at the Rio AGM was palpable. Willie Walsh, IATA’s Director General, acknowledged the severity of the issue, stating, "The challenges around supply chain and MRO capacity are very real and are impacting airline operations globally. We need to see greater transparency and collaboration across the entire aviation value chain to address these bottlenecks."

Several CEOs, speaking anonymously to industry publications on the sidelines of the event, expressed deep frustration. One chief executive from a major European legacy carrier reportedly lamented, "We are in a situation where we have paying passengers, a strong market, but we can’t fully capitalize because half a dozen of our aircraft are sitting on the tarmac waiting for an engine or a specific component. It’s infuriating, and it feels like we are at the mercy of our suppliers." Another CEO from a rapidly expanding low-cost carrier in Asia highlighted the competitive disadvantage, "Our growth strategy is directly tied to fleet expansion. When deliveries are delayed by months, and our existing fleet is less reliable due to parts availability, it slows everything down. Our competitors face similar issues, but the aggregate impact is a drag on the entire industry’s potential."

The discussions extended beyond financial implications to operational resilience. Airlines are being forced to build in more buffer time, adjust schedules, and even cancel flights, leading to passenger inconvenience and reputational damage. The lack of predictability in parts delivery and maintenance turnaround times makes robust operational planning incredibly difficult.

Manufacturer’s Perspective and Challenges

While airlines cast a critical eye on their suppliers, engine and component manufacturers face their own formidable challenges. They, too, are grappling with the repercussions of the pandemic and subsequent global economic shifts. The rapid rebound in air travel caught many off guard, as production lines had been scaled back significantly during the downturn. Ramping up production of complex aerospace components is not an overnight process.

Manufacturers often cite:

- Raw Material Shortages: Access to specialized alloys, rare earth metals, and other crucial raw materials has been inconsistent, impacted by geopolitical events and disrupted global trade routes.

- Labor Shortages: The aerospace manufacturing sector, like many others, lost skilled workers during the pandemic and is struggling to recruit and train new talent quickly enough to meet demand. This affects everything from the factory floor to specialized MRO technicians.

- Supply Chain Resilience: The multi-tiered aerospace supply chain, stretching across continents, proved vulnerable. A single bottleneck at a small, specialized supplier can hold up production for major OEMs.

- Engineering Challenges: For new-generation engines, identifying and implementing solutions for early-life durability issues requires extensive testing, certification, and often a redesign of specific components, which is a time-consuming process.

Manufacturers generally acknowledge the issues and emphasize their commitment to increasing output and improving service. Companies like Pratt & Whitney and CFM International have publicly outlined strategies to boost spare parts production and enhance MRO network capacity, but these initiatives require time to yield significant results.

A Historical Context: Post-Pandemic Supply Chain Woes

The current crisis is not an isolated event but rather an exacerbation of pre-existing vulnerabilities amplified by the COVID-19 pandemic. Before 2020, the aviation supply chain operated on a relatively lean, just-in-time model. When air travel plummeted, production orders for new aircraft and spare parts were drastically cut, leading to layoffs and factory shutdowns across the supply chain.

The unexpected speed and strength of the travel rebound in 2022 and 2023 created an unprecedented demand shock. Manufacturers, who had downsized their operations, found it incredibly difficult to scale back up to meet this sudden surge. The cumulative effect is a global backlog for everything from new aircraft orders to routine spare parts. This timeline of disruption highlights a critical lesson in industrial resilience and the need for more robust, perhaps less lean, supply chain models in strategic sectors like aviation. The challenges faced at the Rio AGM are, in many respects, the delayed fallout of decisions made during the depths of the pandemic.

The Ripple Effect: Impact on Passengers and Operations

The implications of these supply chain and MRO bottlenecks extend beyond airline balance sheets to the traveling public. Reduced fleet availability means airlines have fewer aircraft to operate their planned schedules. This can lead to:

- Higher Fares: With constrained capacity and strong demand, the basic economics of supply and demand dictate higher ticket prices for consumers.

- Fewer Flight Options: Airlines may be forced to reduce frequencies on certain routes or delay the launch of new services, limiting choices for travelers.

- Increased Delays and Cancellations: With less operational flexibility, an unexpected AOG incident can quickly cascade into widespread delays and cancellations, impacting travel plans and customer satisfaction.

- Reduced Reliability: The overall dependability of air travel can suffer as airlines struggle to maintain consistent schedules.

For airline operations teams, the challenge is immense. They are constantly juggling aircraft assignments, crew schedules, and passenger re-bookings, often making real-time decisions based on uncertain parts delivery timelines. This operational strain can also impact employee morale and lead to increased costs for passenger compensation and re-accommodation.

Looking Ahead: Industry Calls for Collaboration and Solutions

The Rio AGM concluded with a clear mandate for greater collaboration and transparency across the aviation value chain. While airlines expressed their frustrations, there was also an acknowledgment that a sustainable solution requires collective effort. IATA, as the industry’s advocate, is expected to play a crucial role in facilitating dialogue between airlines, OEMs, MRO providers, and regulatory bodies.

Potential solutions and areas of focus include:

- Increased Investment in MRO Capacity: Both airlines and independent MRO providers need to invest in expanding facilities, tooling, and skilled labor.

- Enhanced Supply Chain Visibility: Implementing advanced digital tools to track parts and materials throughout the supply chain can help identify and mitigate bottlenecks proactively.

- Long-Term Contracting and Forecasting: More collaborative long-term planning between airlines and manufacturers can help stabilize demand signals and enable better production scheduling.

- Design for Maintainability: Future aircraft and engine designs should prioritize ease of maintenance and component durability to reduce the burden on the MRO ecosystem.

- Regulatory Flexibility: Regulators might need to consider temporary flexibilities in certain maintenance schedules or parts certifications, without compromising safety, to ease immediate pressures.

- Shared Inventory Pools: The concept of airlines sharing common spare parts inventory, perhaps facilitated by manufacturers, could reduce individual airline exposure to AOG events.

The Power Dynamic Shift

Ultimately, the IATA AGM in Rio underscored a significant shift in the power dynamics within the aviation industry. For decades, airlines, as the primary customers, held considerable sway over manufacturers. However, the unique circumstances of the post-pandemic recovery, coupled with the complexity and specialized nature of modern aerospace manufacturing, have tilted the balance. Engine and parts makers, facing their own supply-side constraints, now dictate terms to a greater extent, leaving airlines in a reactive position.

The challenge for the industry going forward is to re-establish a more equitable and collaborative relationship. Without a stable and predictable supply of engines and parts, the airline industry’s ability to grow, innovate, and reliably serve the global traveling public will remain significantly hampered. The ultimate debrief from Rio is a stark reminder that the health of the aviation ecosystem depends not just on robust airlines, but on a resilient and responsive entire value chain, from design and manufacturing to maintenance and operations. The coming years will reveal whether the calls for collaboration from Rio translate into concrete actions that restore equilibrium and foster sustainable growth for all stakeholders.