The Evolution of the "Coupon Book" Reward Model

The transition toward credit-based rewards is a strategic move by card issuers to manage "breakage"—a financial term referring to the percentage of rewards or credits that go unredeemed by consumers. In the past, premium cards justified high annual fees primarily through travel insurance, lounge access, and high point-multipliers on spending. However, as the market became saturated, issuers began offering specific merchant credits to differentiate their products and create "stickiness" within the consumer’s lifestyle.

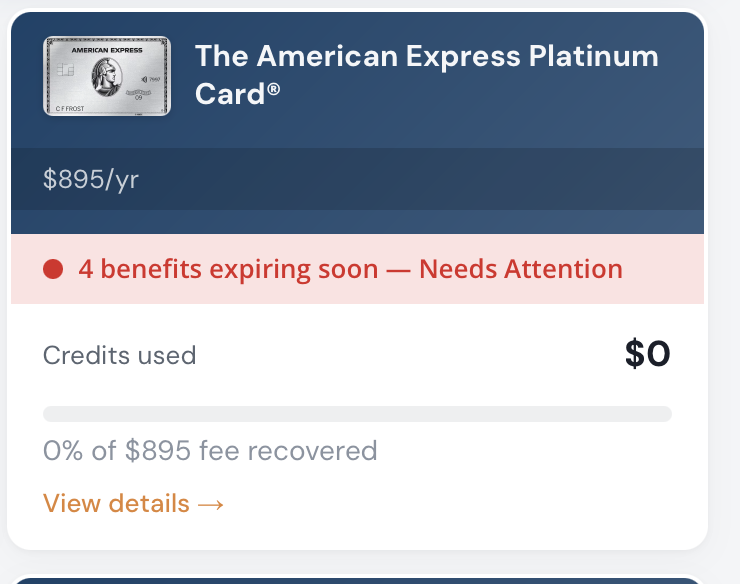

For example, the American Express Platinum Card, which carries a $695 annual fee, offers over $1,500 in potential value through various credits. However, these are fractured into small increments: a $20 monthly digital entertainment credit, a $15 monthly Uber credit, and semi-annual credits for luxury retailers like Saks Fifth Avenue. This model requires a high level of engagement from the consumer. For the bank, this ensures that the card remains "top of mind" and "top of wallet," as users must frequently check their accounts or visit specific merchants to extract the promised value.

Critical Deadlines and the Mid-Year Crunch

The end of June represents a critical juncture for cardholders because many of the most valuable credits are issued on a semi-annual basis. Credits that refreshed on January 1 are set to expire on June 30, meaning any unused balance will vanish at midnight. This creates a surge in consumer activity in late June as cardholders scramble to make purchases they might not have otherwise prioritized.

Common benefits facing the June 30 deadline include:

- Retail Credits: Many premium cards offer $50 to $100 in credits for specific retailers (such as Saks Fifth Avenue or Dell) that refresh every six months.

- Dining and Lifestyle Perks: Newer partnerships, such as those between American Express and the reservation platform Resy, often include quarterly or semi-annual dining credits.

- Travel and Hotel Credits: High-tier cards, including certain offerings from Bilt Rewards and the Chase Sapphire line, provide annual or semi-annual credits for bookings made through their respective travel portals.

Financial experts note that the "trick" to maximizing these cards is to integrate the credits into existing spending patterns. When consumers engage in "revenge spending"—buying unnecessary items simply to utilize a credit—the financial benefit of the card is often neutralized by the out-of-pocket cost of the remaining balance.

Technological Solutions for Reward Management

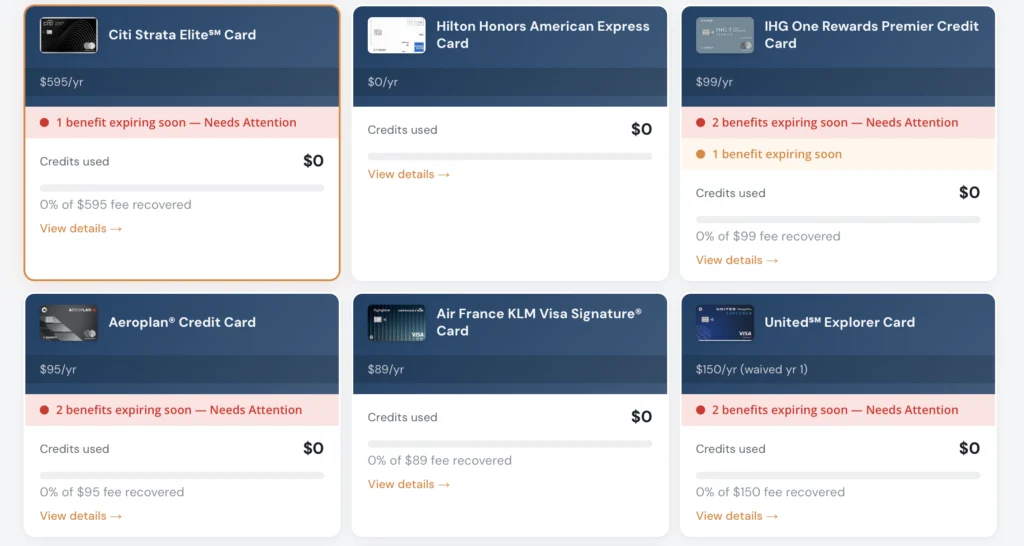

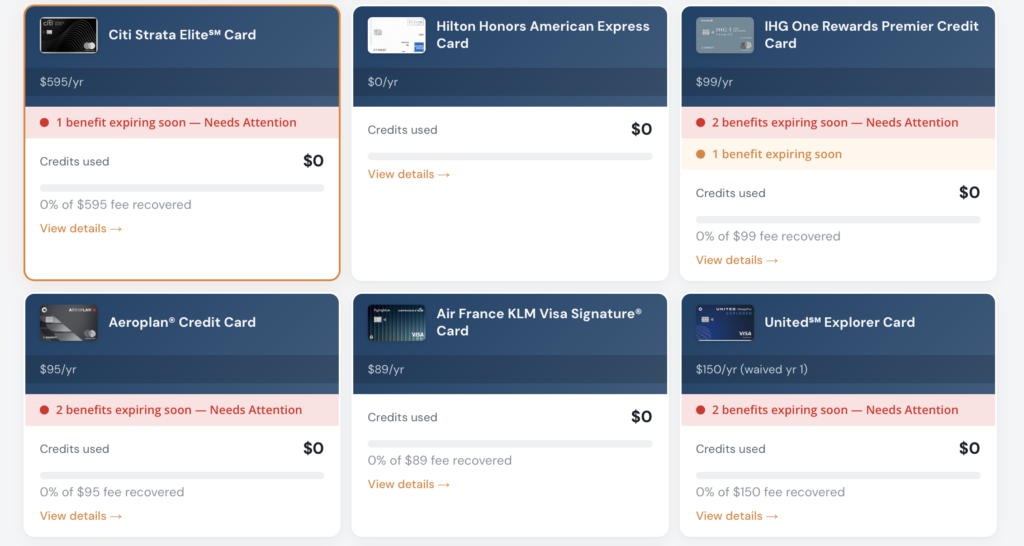

As the complexity of managing multiple "coupon" benefits grows, a secondary market for tracking tools has emerged. Managing a single card’s benefits is manageable, but for "power users" or families who maintain a portfolio of three or more premium cards, the mental overhead can be significant.

Tools such as the Thrifty Traveler credit card benefits tracker have become essential for the modern rewards enthusiast. These platforms allow users to input their specific card inventory and receive automated alerts regarding upcoming expiration dates. By providing a centralized dashboard, these tools mitigate the risk of forgetting a $50 or $200 credit that could significantly impact the net cost of the card’s annual fee.

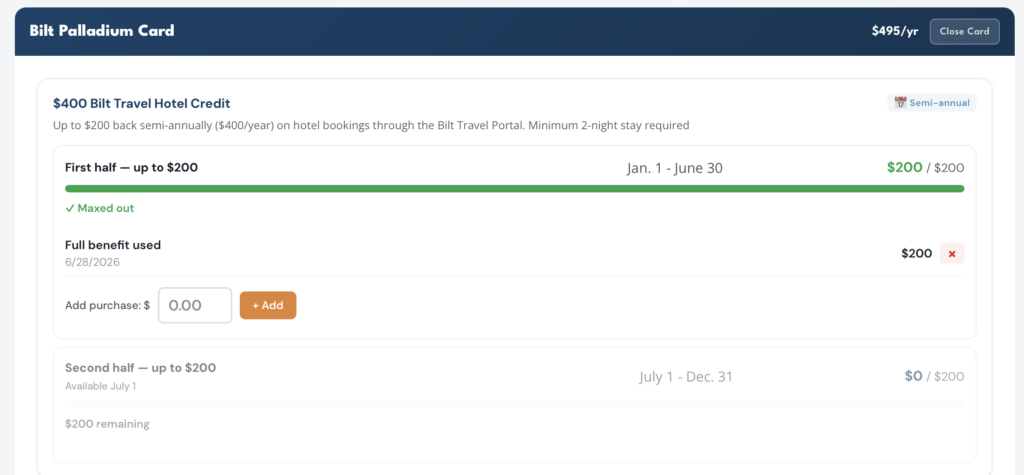

In a recent case study of benefit utilization, a cardholder managed to stack a $200 semi-annual hotel credit with a $100 monthly allowance on a premium Bilt-affiliated card. By strategically pivoting when a primary travel goal (a trip to Thailand) proved difficult to book through the issuer’s portal, the user was able to secure a two-night stay in Austin, Texas, for a total out-of-pocket cost of just over five dollars. This highlights the necessity of flexibility; if a primary use case for a credit is unavailable, cardholders must be prepared to "pivot" to a secondary, pre-planned expense to ensure the credit does not go to waste.

The Financial Logic of Breakage and Consumer Behavior

From the perspective of the financial institution, the "coupon book" model is a win-win. If a customer uses the credit, the bank has successfully driven traffic to a partner merchant (likely earning a referral fee or strengthening a corporate partnership). If the customer fails to use the credit, the bank retains the cash value while still having collected the annual fee upfront.

Industry data suggests that a significant portion of cardholders do not maximize their credits. According to various consumer advocacy reports, "benefit fatigue" is a growing trend. This occurs when the effort required to track and redeem small, fragmented credits outweighs the perceived value of the reward. Consequently, many users may pay a $600+ annual fee but only recoup $200 in actual value, effectively providing the bank with a high-margin profit on the membership fee.

Furthermore, the "portal" requirement—where credits must be used through the bank’s own travel or shopping website—serves as another hurdle. Travel portals often have different pricing than booking direct, and their inventory can be more limited. As seen in the Austin hotel example, users often have to settle for "non-glamorous" options to ensure they don’t lose the credit, illustrating the trade-off between convenience and maximum value.

Chronology of a Reward Cycle

To understand the rhythm of the modern credit card user, one must look at the annual "benefit calendar":

- January 1: The "Grand Reset." Annual and first-half semi-annual credits become available.

- March 31: First-quarter credits (such as those for dining or specific retail categories) expire.

- June 30: The mid-year deadline. This is often the most significant date, as it marks the expiration of semi-annual hotel, retail, and lifestyle credits.

- July 1: The "Second Half" begins. A new set of semi-annual credits is issued.

- September 30: Third-quarter credits expire.

- December 31: The final deadline for all annual and fourth-quarter benefits. This is typically the busiest time for "credit burning," as users realize they have unused travel or incidental credits remaining.

Broader Implications for the Credit Industry

The shift toward these benefits reflects a broader economic trend: the "subscription-ization" of finance. Banks are no longer just lending money; they are acting as lifestyle curators. By partnering with brands like Lululemon, Equinox, Uber, and various airline groups, banks are attempting to embed themselves into the daily routines of their high-net-worth clients.

However, some analysts warn of a potential "race to the bottom." If every premium card offers a similar suite of "coupons," the cards become commodities. Consumers may begin to churn cards more frequently—opening them for the initial sign-up bonus and the first year of credits, then closing them when the "work" of managing the benefits becomes too burdensome.

For the consumer, the advice remains consistent: treat credit card benefits like a business ledger. If the time spent tracking and redeeming credits exceeds the monetary value gained, or if the credits encourage spending at merchants the consumer would not otherwise frequent, the card may not be a sound investment.

Conclusion: Preparing for the June 30 Deadline

As the clock ticks toward the end of the second quarter, cardholders are encouraged to perform a "wallet audit." This involves logging into each card issuer’s app, checking the "Benefits" or "Rewards" tab, and confirming which credits have been utilized.

The strategy for the final 24 to 48 hours of the quarter should be focused on utility. If a hotel credit remains, booking a future trip—even if it is a modest domestic stay—is preferable to letting the credit expire. If a retail credit remains, purchasing household staples or gifts can ensure the value is captured. In the current economy, where annual fees continue to climb, the difference between a "valuable" credit card and an "expensive" one often comes down to the cardholder’s ability to stay organized and execute their redemptions before the deadline passes. Use them or lose them; the choice rests entirely with the consumer.