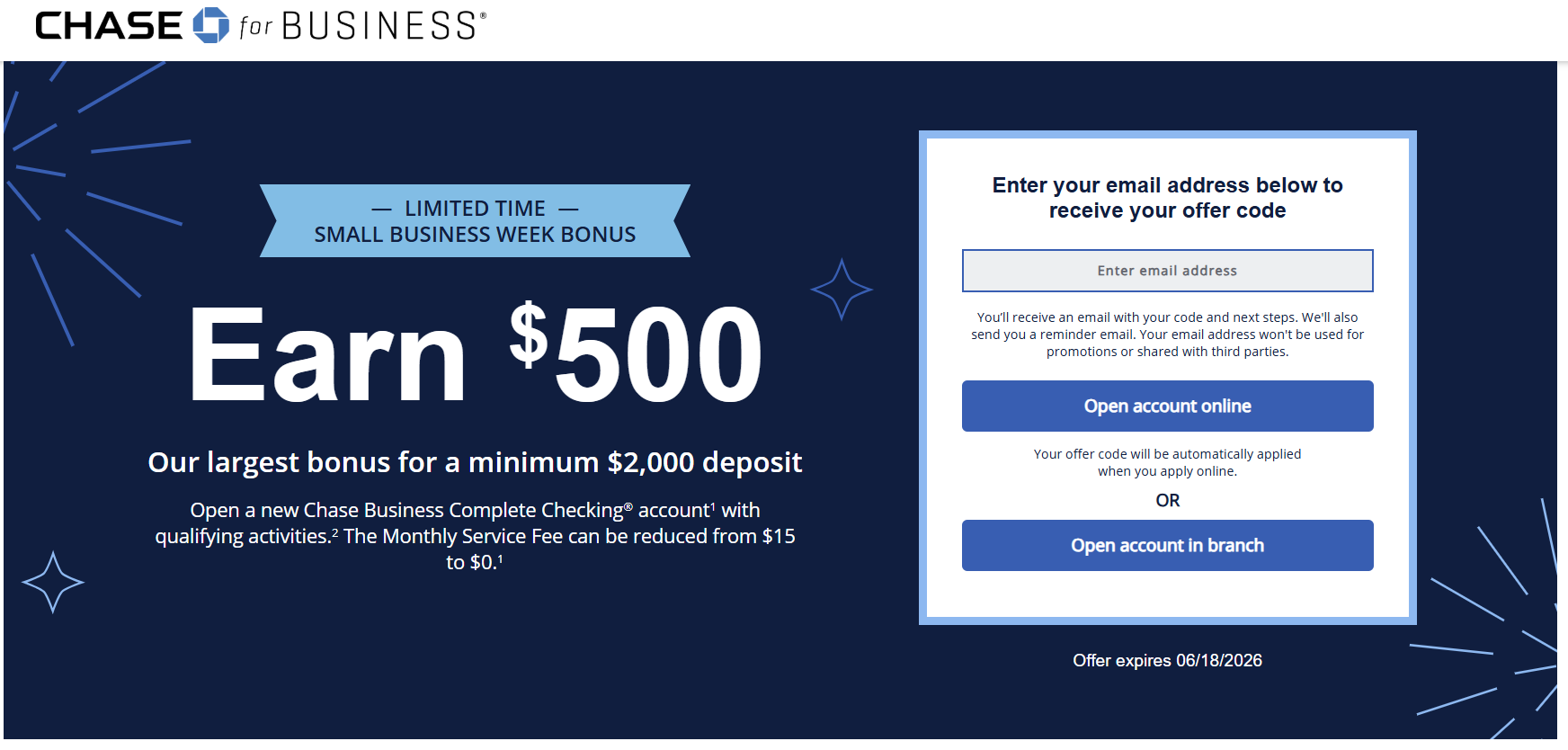

JPMorgan Chase & Co. has officially launched a highly competitive promotional incentive targeting small business owners and entrepreneurs, offering a $500 cash bonus for new Chase Business Complete Checking® account enrollments. This limited-time offer distinguishes itself from previous iterations by requiring a significantly lower capital commitment than traditional high-tier business banking promotions. To qualify for the incentive, new account holders must deposit at least $2,000 in new money within 30 days of account opening and maintain that balance for a minimum of 60 days. Industry analysts note that the ratio of the bonus to the required deposit—effectively a 25% return on the initial $2,000 investment—represents one of the most aggressive customer acquisition strategies seen in the national commercial banking sector this year.

Strategic Overview of the Incentive Structure

The current promotion is structured to attract a broad spectrum of business entities, ranging from established corporations to independent contractors operating as sole proprietorships. Unlike many high-value banking bonuses that require a complex series of recurring direct deposits or massive capital outlays often exceeding $20,000, this Chase offer focuses on accessibility. The primary requirements involve three distinct phases: the enrollment phase, the funding phase, and the activity phase.

During the enrollment phase, prospective clients must apply through a specific promotional link or present a unique coupon code at a physical Chase branch location. Upon successful account opening, the funding phase begins, requiring the injection of "new money"—defined as funds not currently held by Chase or its affiliates—totaling $2,000 or more. This deposit must be completed within 30 days of the account’s inception. Following the deposit, the account holder must maintain the $2,000 balance for 60 days. Finally, the activity phase requires the completion of five qualifying transactions within the first 90 days. These transactions can include debit card purchases, ACH payments, or wire transfers.

Chronology of the Account Lifecycle and Bonus Payout

The timeline for securing the $500 bonus is rigid, and adherence to the schedule is paramount for eligibility. The process typically unfolds over a four-month period from the date of application to the date of funds disbursement.

- Day 0 (Account Opening): The applicant submits their documentation and uses the promotional code. For sole proprietors, this often involves using a Social Security Number (SSN), while more formal entities use an Employer Identification Number (EIN).

- Days 1–30 (Funding Window): The $2,000 minimum deposit must be initiated and cleared. It is critical to note that the 60-day maintenance clock begins at the moment of enrollment, not the moment of deposit. Consequently, if a user deposits the funds on Day 25, they only need to maintain that balance until Day 60 to satisfy the bank’s requirements, effectively reducing the capital "lock-up" period to approximately 35 days.

- Days 1–90 (Transaction Window): The account holder must perform at least five qualifying transactions. These are most commonly executed via the provided business debit card for standard business expenses.

- Day 61 (Maintenance Completion): Once the account has remained open for 60 days with the requisite balance maintained, the primary financial requirement is satisfied.

- Post-Day 60 (Verification and Payout): After all requirements are met, Chase typically reviews the account for compliance. According to the terms and conditions, the $500 bonus is generally deposited into the account within 15 days of the final requirement being verified.

Comparative Data and Financial Analysis

When compared to standard market offerings, the Chase $500 Business Checking bonus is an outlier in terms of yield. To put the $500 bonus into perspective, a traditional high-yield business savings account offering a 4.00% Annual Percentage Yield (APY) would require a $2,000 balance to remain untouched for over six years to generate the same $500 return. In this promotional context, the same return is achieved in approximately two months.

Historically, Chase has offered a $300 bonus for the same $2,000 deposit. The increase to $500 represents a 66% enhancement in the value proposition for the consumer without an increase in the capital requirement. Furthermore, Chase’s higher-tier offers, such as those reaching $750 or $1,000, typically require deposits of $20,000 or $30,000, respectively. For small businesses with limited liquidity, the $2,000 threshold provides a significantly lower barrier to entry while maintaining a high reward.

The "yield on deposit" for this specific offer is approximately 25% for the holding period. On an annualized basis, this is a theoretical return that far outstrips any conventional investment vehicle currently available in the low-risk banking sector.

Eligibility Criteria for Diverse Business Entities

A notable feature of this promotion is its inclusivity regarding business structures. JPMorgan Chase has clarified that the offer is available to a wide variety of legal entities. This includes:

- Sole Proprietorships: Individuals doing business under their own name or a "Doing Business As" (DBA) name. These applicants can use their personal Social Security Number for the application, making it accessible for freelancers and "gig economy" workers.

- Limited Liability Companies (LLCs): Both single-member and multi-member LLCs are eligible, provided they have the necessary formation documents and an EIN.

- Corporations and Partnerships: More complex legal entities are also eligible, though they may require more extensive documentation during the in-branch or online application process.

Current Chase personal banking customers are eligible for this business bonus, provided they do not already have an existing Chase business checking account and have not received a business checking bonus within the last two years. Additionally, the account must not have been closed with a negative balance within the last three years.

Fee Structure and Maintenance Requirements

While the $500 bonus is a significant draw, prospective account holders must also consider the ongoing cost of maintaining a Chase Business Complete Checking® account. The account carries a $15 monthly maintenance fee, which can erode the value of the bonus if not waived. Chase provides several avenues for customers to avoid this fee:

- Minimum Daily Balance: Maintaining a minimum daily balance of $2,000 or more in the account.

- Chase Ink® Business Credit Card Spend: Linking a Chase Ink® Business credit card and spending at least $2,000 on that card during the billing cycle.

- Qualifying Deposits: Receiving at least $2,000 in qualifying deposits from QuickAccept℠ or other eligible Chase merchant services.

- Military Status: Providing proof of active or veteran military status.

For most small business owners, maintaining the $2,000 balance used for the bonus qualification is the most straightforward method to ensure the account remains fee-free indefinitely.

Broader Economic Implications and Competitive Landscape

The launch of this aggressive promotion comes at a time when traditional brick-and-mortar banks are facing increased competition from digital-only "fintech" banks like Mercury, Brex, and Bluevine. These digital competitors often offer fee-free structures and high interest rates on balances, forcing established giants like JPMorgan Chase to utilize large cash incentives to maintain their market share in the small business sector.

Small businesses are considered "sticky" customers in the banking industry. Once a business establishes its checking account, integrates its payroll, and sets up its merchant services with a bank, the cost of switching to a competitor becomes high. By offering a $500 incentive for a relatively low deposit, Chase is likely calculating that the long-term lifetime value of these business customers will far outweigh the initial $500 acquisition cost.

Furthermore, the focus on small business accounts aligns with broader economic trends. Despite fluctuating interest rates and inflationary pressures, the small business sector remains a primary driver of employment and economic activity in the United States. By capturing these customers early in their lifecycle—especially sole proprietors and new LLCs—Chase positions itself as the primary lender and financial partner as these businesses scale.

Official Stance and Market Response

While JPMorgan Chase does not typically comment on the specific performance metrics of individual promotional campaigns, the bank’s quarterly earnings reports consistently emphasize the growth of its "Business Banking" segment as a key pillar of its consumer and community banking division. In recent statements, bank executives have highlighted their commitment to supporting small business resilience through localized branch support and digital innovation.

Market response to the $500 offer has been overwhelmingly positive among financial analysts and consumer advocacy groups. Financial experts suggest that for businesses with idle cash, moving $2,000 into a Chase account for a 60-day period is a low-risk strategy with a high guaranteed payout. However, they also caution users to ensure they complete the five required transactions, as failure to meet any single requirement will result in the forfeiture of the entire $500 bonus.

Final Considerations for Prospective Applicants

Before applying, business owners are encouraged to gather necessary documentation, which typically includes a government-issued ID, Social Security Number or EIN, and business formation documents (such as Articles of Organization or a Business License). While the application can often be completed online, some entities—particularly those with multiple owners—may be required to visit a branch to finalize the account opening.

As the banking landscape continues to evolve, these types of high-value, low-barrier promotions serve as a critical tool for business owners to maximize their liquid assets. With a clear path to a $500 return on a $2,000 deposit, this Chase offer currently stands as a benchmark for value in the commercial banking sector, reflecting the intense competition for the American small business dollar.